Invesco: Investing in the European upper middle market

European upper middle market private credit offers defined contribution pension investors yield, diversification, and stability by combining directly originated and syndicated loans across larger, more resilient corporate borrowers.

By Michael Craig, Head of European Senior Secured Loans, and Raman Rajagopal, MD & Senior Client Portfolio Manager - Private Credit, both at Invesco

As DC pension investors search for ways to diversify beyond traditional asset classes, European private credit has become an increasingly relevant area of opportunity. Within this universe, lending to upper middle market companies — larger, well-capitalized businesses with stronger balance sheets — has gained prominence.

Upper middle market borrowers can offer enhanced yield relative to traditional fixed income, lower correlation to public markets, floating-rate structures that help hedge inflation, and portfolio diversification both within fixed income exposure and across broader asset allocations.

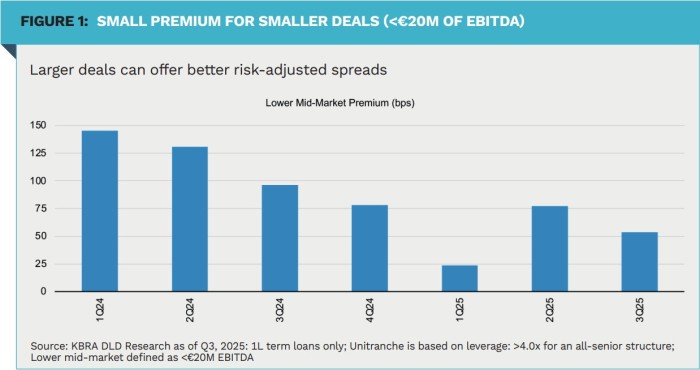

We believe upper middle market debt is often associated with companies that exhibit relatively strong and stable balance sheets profiles. On a risk-adjusted basis, larger European companies may offer nearly the same spread as smaller companies while aiming to provide greater downside protection. In other words, lending to smaller European companies does not tend to deliver meaningfully higher spread to compensate for the additional risk.

The key to evaluating this opportunity

For DC pension plans evaluating this opportunity set, the strategic insight lies in recognizing how upper middle market borrowers toggle between syndicated and direct lending depending on pricing, speed, and flexibility. From our perspective, investors focused on lending to these companies should consider incorporating both access points in their approach.

Direct lending and syndicated loans

Historically, European corporate private credit was segmented between syndicated loans for larger companies and direct lending for smaller firms.

- The syndicated market involves loans originated by banks and then shortly thereafter distributed to institutional investors. Given the broad market awareness and borrower size, syndicated loans thereafter maintain a strong secondary market and regular liquidity.

- Direct lending, by contrast, involves non-bank lenders originating loans directly with borrowers. These direct deals offer a spread premium but come with limited secondary liquidity, meaning lenders typically hold them through maturity

Following the Global Financial Crisis, regulatory changes and capital requirements reduced bank lending capacity, opening the door for non-bank lenders. As private credit markets expanded, direct lending funds accumulated significant dry powder, enabling them to target larger companies.

Upper middle market borrowers use both types of solutions

Today, European upper middle market borrowers consider debt solutions from both markets. For some borrowers, direct origination is preferable given the speed, certainty, and flexibility of these facilities. For others, the scale of the syndicated loan market and pricing make it the preferred solution. And many may toggle between the two based on pricing/spread differentials at any moment in time.

- In times of weak issuance in syndicated loan markets, spreads for new deals widen (as was the case in 2022), and consequently, direct lending deal activity increases.

- Conversely, in times when the syndicated new issue market is strong and spreads are dropping (as observed in 2024), many upper middle market borrowers shift away from the direct lending market in favor of syndicated markets.

Investors who restrict themselves to only one channel risk reduced deployment, diminished yield capture, and weaker alignment with borrower behavior.

Because upper middle market borrowers frequently shift between these financing types, investors who restrict themselves to only one channel risk reduced deployment, diminished yield capture, and weaker alignment with borrower behavior.

Direct lending to upper middle market companies typically delivers an illiquidity premium of 100–300 basis points relative to syndicated loans. Meanwhile, syndicated loans offer liquidity and broader market access. For investors, combining both provides two advantages: the ability to remain consistently deployed and the opportunity to capture the premium associated with lending to larger, more stable companies through private structures. The integration of these channels within a single strategy aligns investor positioning with how upper middle market companies finance themselves.

Value drivers in European upper middle market lending

Sourcing and diligence are two critical value drivers in lending capital to European upper middle market companies.

- From a sourcing perspective, we believe the most important consideration relates to the scale of relationships with the largest deal sponsors in the market, as these are the entities which own firms in the upper middle market.

- From a diligence perspective, deep sector expertise helps ensure an understanding of the unique dynamics and risks of each industry when evaluating potential investments. Extensive familiarity with borrowers enhances the ability to assess creditworthiness.

Conclusion

Through direct lending structures, investors may benefit from an illiquidity premium while broadly syndicated structures can offer flexible deployment and periodic liquidity. By combining both types of loans into a single strategy, investors can gain access to the strongest companies within the European upper middle market.

|

SUMMARY European private credit offers DC pensions enhanced yield, diversification, and stability. Larger upper middle market companies can provide stronger risk-adjusted returns and more resilient cash flows. Upper middle market borrowers toggle between syndicated and direct loans based on pricing and flexibility. By combining both types of loans into a single strategy, investors can gain access to the strongest companies within the European upper middle market. |

|

Investment risks The value of investments and any income from them may fluctuate (this may partly be due to exchange rate movements), and investors may not get back the full amount originally invested. Important Information This marketing communication is intended solely for use by the Dutch professional press. It is not intended for, and must not be distributed to, the general public. All data is as of 20/03/2026 unless otherwise stated. This is marketing material and not financial advice. It is not intended as a recommendation to buy or sell any asset class, security, or strategy. Legal requirements regarding the impartiality of investment recommendations or strategies do not apply. Nor are there any restrictions on trading prior to publication. Views and opinions are based on current market conditions and are subject to change. Issued by: Invesco Management S.A., President Building, 37A Avenue JF Kennedy, L-1855 Luxembourg, regulated by the Commission de Surveillance du Secteur Financier (CSSF), Luxembourg. EMEA5331500 |

Read the full article in Financial Investigator magazine