ILX Management: Achieving SDGs & climate targets in emerging markets

ILX Management: Achieving SDGs & climate targets in emerging markets

With their long-term emerging market experience and status, multilateral development banks and development finance institutions are key in providing institutional investors with investment opportunities that contribute to reaching the SDGs and climate targets and closing the existing funding gap.

By Manfred Schepers, CEO of ILX Management

The world is facing a climate crisis. Floods, fires and other climate-related disasters are ever-present in the news, amplifying the urgency to take collective action to meet the SDGs and climate targets (G20 Triple Agenda Vol.2, 2023). These inequalities and climate events affect the whole world, but more acutely the developing countries, which are excessively exposed to the consequences of climate change and expected to account for two-thirds of the global greenhouse gas emissions’ growth. There is universal recognition that scaling up development finance in emerging markets (EMs) is an urgent global imperative, needed to reduce emissions and mitigate the consequences of climate change that countries are facing. Luckily, it also provides a solid investment opportunity for institutional investors globally.

The Triple Agenda Report, 2023

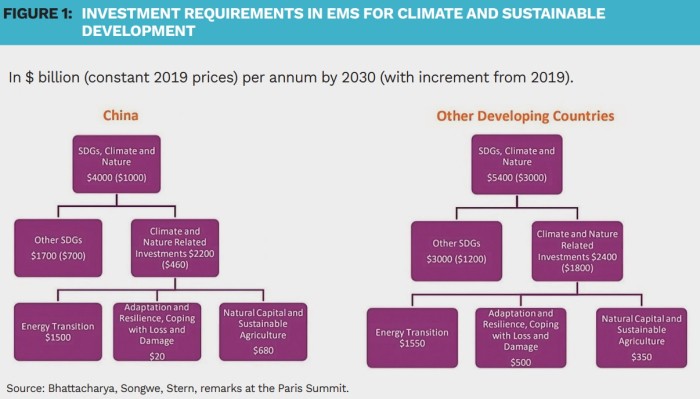

In the 2023 Delhi Declaration, the G20 Leaders highlighted the need for greater investments to be able to meet international objectives, such as the SDGs and the Paris Agreement’s climate targets, specifically in EMs. Governments and public finance channels do not have the balance sheet capacity to cover the required funding for these objectives, which is estimated to be around $ 4 trillion between now and 2030 (OECD, 2023). Private investment flows from institutional investors are also lagging behind.

EMs lack well-established, deep local bond and equity markets and have limited access to international capital markets, whilst the international banking systems from the US, Europe and Asia have largely withdrawn from providing long-term finance in these regions, after the Great Financial Crisis 15 years ago.

Development finance offers a scalable investment opportunity with market-equivalent risk-adjusted returns that are compelling versus alternative EM bond and credit markets.

Recent work, such as the G20 Triple Agenda report, has established that multilateral development banks (MDBs) and development finance institutions (DFIs), including the World Bank’s International Finance Corporation (IFC), European Bank for Reconstruction and Development (EBRD) or the Dutch entrepreneurial development bank (FMO), play a central role in closing the finance gap on the SDGs and climate targets across EMs. The MDBs and DFIs are uniquely equipped and positioned to tackle these challenges at a large, systemic scale.

These institutions were established decades ago with committed capital from leading developed countries and government shareholders. They had a clear goal of providing long-term development finance in markets where private finance was lacking. Over time, their missions have evolved to encompass the broader objectives of the SDGs, especially to address climate change mitigation and adaptation challenges in EMs.

Today, these institutions have over fifty years of investment experience across EMs, in projects that provide direct and measurable SDG- and climate-related results. They also have environmental and social safeguards in place. These years of experience and local presence have made these institutions into multi-faceted experts in credit, country, sector, and sustainability-related factors when it comes to investing in EMs.

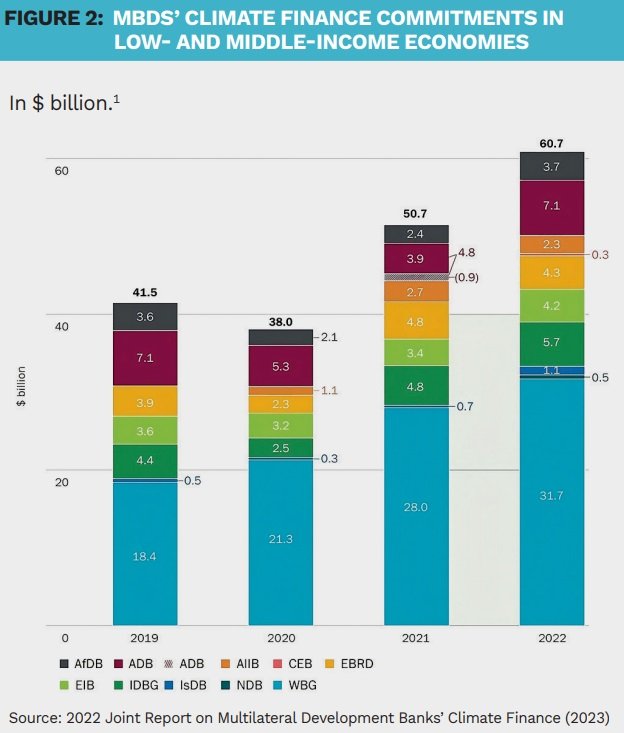

MDBs recently acknowledged their responsibility at the World Bank’s 2023 Annual Meeting in Marrakech. They are committed to strengthening their collaboration and individual actions as well as expanding their lending capacity to be able to increase their positive impact. These words have proven to carry some weight – the MDBs announced they collectively reached a new record high of nearly $ 60 billion in climate finance in 2022 in low- and middle-income countries (Climate Finance joint report by the MDBs, 2023). This increased responsibility will be reiterated during the COP28 held in UAE at the end of the year.

Climate Finance joint report by the MDBs, 2023

To secure the necessary $ 4 trillion in financing to achieve the SDGs and climate targets, MDBs and DFIs view the inclusion of private finance – known as ‘mobilization’ – as one of their most important tools. By sharing, transferring or selling part of their own exposures to institutional investors, they free up their own balance sheet, which can then be used for additional risk capacity to move toward new markets and invest in new projects.

Private capital mobilization currently amounts to $ 60 billion annually, but it will need to be scaled up to at least $ 240 billion annually by 2030 if the SDGs and climate targets are to be reached (G20 Triple Agenda Vol.2, 2023).

The lack of credit statistics transparency can be addressed by initiatives such as the publication of the Global Emerging Markets Risk Database.

From an investor perspective, this development finance asset class should not be overlooked. Development finance, through large-scale institutional private debt funds, offers a scalable investment opportunity with market-equivalent risk-adjusted returns that are compelling versus alternative EM bond and credit markets. These returns are largely uncorrelated with public market volatility. It also provides diversification across all EM regions and sectors, and benefits from the highest governance and safeguarding standards of the MDBs and DFIs.

Moreover, being international financial institutions, the MDBs benefit from important privileges and immunities. This includes the preferred creditor treatment (PCT), which is a de facto exemption from transfer restrictions imposed by host countries, and a preferred creditor status (PCS) with respect to sovereign lending. The extensive local experience and status of these MDBs significantly reduce the inherent risks associated with investing in EMs.

Co-financing alongside MDBs and DFIs further provides access to SDGand climate-related results on a project-by-project basis as it enables tracking of the use of proceeds and measuring of the sustainability results of the investments. It gives institutional investors the opportunity to invest through funds in private debt portfolios that, due to their high impact, ESG-safeguarding and granular project-based reporting, can qualify as SFDR Article 9 Funds.

Despite the advantages, high geopolitical and credit risks are often observed as the key hurdles institutional investors face when venturing into this development finance asset class. However, a discrepancy exists between the perceived risk and the actual risk of the projects financed by MDBs, largely caused by the lack of data transparency in development finance.

This lack of credit statistics transparency can be addressed by initiatives such as the publication of the Global Emerging Markets Risk Database. This database, containing 33 years of anonymized credit default statistics from over 10,000 loan obligors, shared by 23 MDBs and DFIs, helps to offer a portrayal of the low credit risks associated with development finance. It has proven to be part of the solution that helps attract much-needed private debt investment into this asset class, by bridging the perception gap between perceived and actual risk.

Improved data transparency in the underlying credit risk of development finance is an important step in scaling-up this asset class. At the same time, the development finance asset class will only be able to significantly grow by creating a broad, harmonized, transparent, predictable and efficient market for these assets. Similar to other large-scale investment asset classes, this needs to be based on a granular understanding of individual risks at the country, sector, obligor and project level.

Development finance assets can only be analyzed and potentially securitized at a portfolio level, if the obligor and project-level risks are fully understood, incorporating the corporate, sector and country-level risks. This is not something new – existing equity, credit, bond and commodity markets have all grown and developed through a granular understanding of the individual risks at the company and project level. The upscaling of development finance will need to follow the same pattern and data transparency will be key to facilitate this.

All in all, MDBs and DFIs will provide institutional investors, through diversified private debt fund structures, with a unique opportunity to invest in stable, well diversified and attractively yielding development finance loan assets. Investors will also get closer to meeting their SDGs and climate targets, and to supporting positive impact in countries and EM regions that most need it. The discussion should not be whether to invest in development finance in EMs or not, but rather when to scale up. It is time to seize this opportunity.

Abbreviations: AfDB: African Development Bank; ADB: Asian Development Bank; AIIB: Asian Infrastructure Investment Bank; CEB: Council of Europe Development Bank; EBRD: European Bank for Reconstruction and Development; EIB: European Investment Bank; IDBG: Inter-American Development Bank Group; IsDB: Islamic Development Bank; NDB: New Development Bank; WBG: The World Bank Group.

|

SUMMARY Multilateral development banks (MDBs) and development finance institutions (DFIs) are uniquely positioned to enable the transition into a low-carbon economy in emerging markets and support the adaptation to the effects of climate change. Co-investing with these development banks in a diversified pool of high-impact projects, provides investors with stable and commercial risk-adjusted returns. Bridging the SDGs and climate funding gaps requires increased private capital flows to Emerging Markets through innovative and efficient fund vehicles. |

Bijlagen

Deel dit bericht

Gerelateerde berichten

-

Lees meer over "Guido Veul (AF Advisors): Steeds minder keuze voor PAB-beleggers"

Lees meer over "Guido Veul (AF Advisors): Steeds minder keuze voor PAB-beleggers"Guido Veul (AF Advisors): Steeds minder keuze voor PAB-beleggers

-

Lees meer over "DNB: Pensioensector zet stappen richting verankering duurzaamheidsrisico's"

Lees meer over "DNB: Pensioensector zet stappen richting verankering duurzaamheidsrisico's"DNB: Pensioensector zet stappen richting verankering duurzaamheidsrisico's

-

Lees meer over "Columbia Threadneedle: Extreem weer is brandstof voor defensie-uitgaven"

Lees meer over "Columbia Threadneedle: Extreem weer is brandstof voor defensie-uitgaven"Columbia Threadneedle: Extreem weer is brandstof voor defensie-uitgaven

-

Lees meer over "DMPM publiceert eerste ESG Report"

Lees meer over "DMPM publiceert eerste ESG Report"DMPM publiceert eerste ESG Report

-

Lees meer over "a.s.r.: Meetmethode voor plasticimpact in beleggingen"

Lees meer over "a.s.r.: Meetmethode voor plasticimpact in beleggingen"a.s.r.: Meetmethode voor plasticimpact in beleggingen

-

Lees meer over "Schroders: ‘Super El Niño’ dreigt nieuwe inflatiegolf aan te jagen"

Lees meer over "Schroders: ‘Super El Niño’ dreigt nieuwe inflatiegolf aan te jagen"Schroders: ‘Super El Niño’ dreigt nieuwe inflatiegolf aan te jagen

-

Lees meer over "Steven Poelhekke: Hoe houden we de klimaattransitie op schema in tijden van oorlog?"

Lees meer over "Steven Poelhekke: Hoe houden we de klimaattransitie op schema in tijden van oorlog?"Steven Poelhekke: Hoe houden we de klimaattransitie op schema in tijden van oorlog?

-

Lees meer over "JSS: Geopolitiek en klimaatverandering kunnen landbouwprijzen opdrijven"

Lees meer over "JSS: Geopolitiek en klimaatverandering kunnen landbouwprijzen opdrijven"JSS: Geopolitiek en klimaatverandering kunnen landbouwprijzen opdrijven

-

Lees meer over "Harry Geels: De vijf denkfouten van Piketty"

Lees meer over "Harry Geels: De vijf denkfouten van Piketty"Harry Geels: De vijf denkfouten van Piketty

-

Lees meer over "EDHEC: Can climate equity investors cope with oil price volatility?"

Lees meer over "EDHEC: Can climate equity investors cope with oil price volatility?"EDHEC: Can climate equity investors cope with oil price volatility?