Fidelity: Macro and multi-assets – time for more perspective

Fidelity: Macro and multi-assets – time for more perspective

This article was originally published in Dutch. This is an English translation.

A favourable macro environment offers opportunities for 2026, but geopolitical shifts, a weakening dollar and structural inflation require sharp risk management and broad diversification.

By Ahmed Salman, Global Head of Macro and Strategic Asset Allocation, Fidelity International

We are entering 2026 with a favourable macroeconomic climate. Economic growth remains resilient and both monetary and fiscal policy are accommodative. Major concerns from the past year – such as persistent core inflation and the impact of high interest rates – are receding. Nevertheless, risks remain: a possible deterioration in the labour market, unexpected rises in inflation, the debate surrounding the independence of the Fed, and the dynamics surrounding AI-driven investments and profit cycles. For the time being, these factors appear to be manageable.

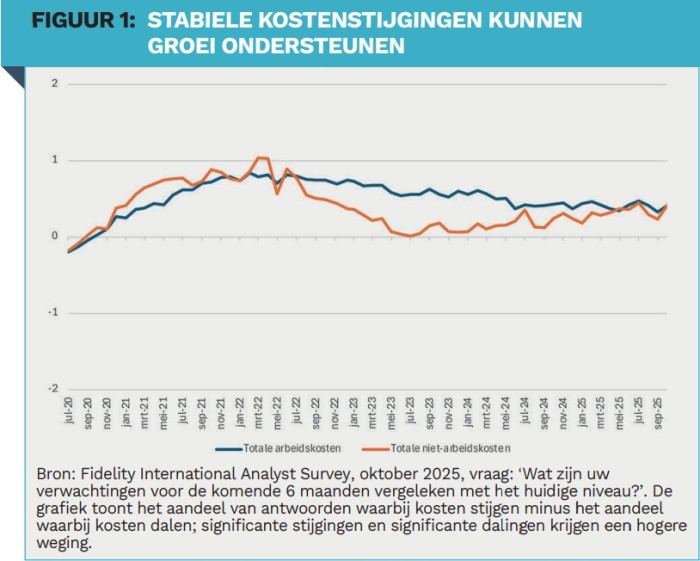

Our investment analysts also see an improved environment. Lower interest rates make financing cheaper and more accessible, while more pro-business policies support companies. Our analysts expect cost increases within the companies they follow to remain largely stable over the next six months, which is favourable for profit growth.

Despite the positive short-term environment, profound structural changes continue to play out. The world is shifting towards greater fragmentation after decades of globalisation. Donald Trump's presidency reflects and reinforces this movement: his policies have resulted in the most restrictive US trade and tariff policy since the Second World War. Although he has distanced himself from his most extreme proposals, the trend remains clearly protectionist.

An important part of this new strategy is the deliberate weakening of the US dollar. The government wants to reduce the trade deficit and direct capital flows towards productive domestic investments, such as factories and infrastructure, rather than US government bonds. The dollar is thus increasingly becoming a policy instrument. Combined with discussions about the independence of the Fed – which will intensify in May 2026 when Jerome Powell steps down – we expect the dollar to weaken further in the coming years.

These structural shifts mean that investors need to take another look at the risks of holding dollar positions. Geopolitical volatility is likely to increase in 2026. Gold offers important protection in this context. The euro is becoming more attractive, partly because the Fed is likely to come under greater pressure to ease further. At the same time, fiscal policy in Europe – such as higher defence spending – is supporting the currency.

Income strategies can help make portfolios more robust. Dividend-focused investments provide stable cash flows and greater diversification beyond the dominant growth and tech stocks. Investors should also take into account long-term changes: the high weighting of the US in global benchmarks makes hedge ratios more important in an environment of a weakening dollar.

We also expect inflation to remain structurally higher. This increases the correlation between equities and bonds, reinforcing the role of alternative sources of diversification: real assets, currencies and absolute return strategies are becoming increasingly relevant.

Identifying risks

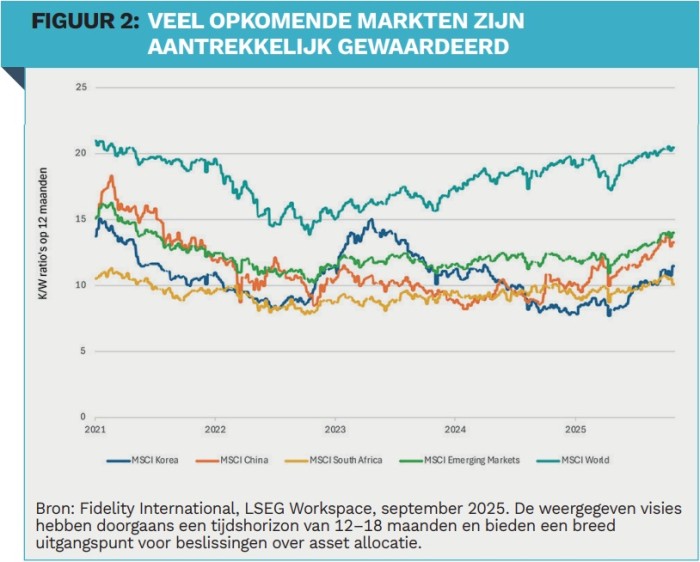

A weaker dollar offers significant opportunities in emerging markets, one of our key themes for 2026.

A weaker dollar offers significant opportunities in emerging markets, one of our key themes for 2026.

In several countries, such as South Korea and South Africa, fundamentals are improving and we see attractive valuations. China remains attractive thanks to broad policy support that creates scope for thematic opportunities.

Local currency bonds from emerging markets, especially in Latin America, also offer high real yields and attractive yield curves. Brazil stands out as a favourite, partly due to healthy macro fundamentals.

As far as corporate bonds are concerned, spreads remain historically tight. The US market is at a later stage of the cycle, which is why we are opting for shorter maturities in a defensive carry strategy. From a multi-asset perspective, high yield is preferred over investment grade, given the solid credit quality and relatively better valuation.

The role of AI

AI remains a driving force behind productivity and profit growth. The market supports high valuations across the entire AI chain, but this is broad and diverse. There are various ways to play the AI theme.

In addition to the large tech companies and chip manufacturers, there are companies that provide infrastructure, platforms and hardware that are essential for AI implementation. Furthermore, there is a growing segment in “physical AI”: robotics, automation and industrial applications, which are expected to grow strongly in 2026.

In addition, there is enormous demand for electricity. Globally, approximately £21 trillion in investment will be needed in electricity grids by 2050, accounting for 9 million kilometres of additional transmission lines.1 Demand for materials such as copper and uranium is rising accordingly.

We want to remain present in all segments of the AI value chain: hyperscalers, chipmakers, but also the relatively inexpensive laggards that are catching up.

A new risk landscape

The positive risk climate is accompanied by fundamental changes that will continue to influence portfolios beyond 2026. Investors need to be more careful about where they take risks, without necessarily sacrificing returns. Despite increased uncertainty, our stance remains constructive: there are plenty of opportunities, provided investors pay attention to macroeconomic and geopolitical imbalances and their impact on portfolios.

1 Global Net Zero Will Require $21 Trillion Investment In Power Grids, BloombergNef, 2023.

|

SUMMARY Accommodative monetary and fiscal policy, combined with solid corporate earnings, supports a positive outlook for equity risk. Emerging market equities appear particularly attractive. The expected depreciation of the US dollar supports emerging market local currency bonds. Preference is given to countries with high real interest rates and attractive valuations. Gold, absolute return strategies and private assets offer important diversification in 2026 portfolios. |

|

Important information Investors should note that the views expressed may no longer be current and may have already been acted upon. The value of investments and the income derived from them may fluctuate, and you/the client may not recover the amount invested. Past performance is no guarantee of future returns. Investments abroad are affected by changes in exchange rates. Investments in emerging markets may be more volatile than those in more developed markets. This information may not be copied or distributed without prior permission. Fidelity provides information about its own products and services only and does not provide investment advice based on personal circumstances, unless otherwise specifically stated by a duly regulated firm in formal communication with the client. Fidelity International refers to the group of companies that form part of the global investment management organisation that provides information about products and services in certain jurisdictions outside North America. This publication is not intended for residents of the United States and is intended solely for persons located in jurisdictions where the relevant funds are authorised for distribution or where such authorisation is not required. Unless otherwise indicated, all products are offered by Fidelity International and all opinions and views expressed herein are those of Fidelity. Fidelity, Fidelity International, the Fidelity International logo and the F symbol are registered trademarks of FIL Limited. Trademarks, copyrights and other intellectual property of third parties are and remain the property of their respective owners. Issued by FIL (Luxembourg) S.A., authorised and regulated by the CSSF (Commission de Surveillance du Secteur Financier). |

Read the article in Financial Investigator magazine here

Attachments

Share this post!

Related posts

-

Read more about "A lack of risk appetite in Europe"

Read more about "A lack of risk appetite in Europe"A lack of risk appetite in Europe

-

Read more about "J.P. Morgan Private Bank: Mid-Year Outlook 2026"

Read more about "J.P. Morgan Private Bank: Mid-Year Outlook 2026"J.P. Morgan Private Bank: Mid-Year Outlook 2026

-

Read more about "Han Dieperink: The bull market is only halfway through"

Read more about "Han Dieperink: The bull market is only halfway through"Han Dieperink: The bull market is only halfway through

-

Read more about "Schroders: Hogere inflatie en lagere economische groei"

Read more about "Schroders: Hogere inflatie en lagere economische groei"Schroders: Hogere inflatie en lagere economische groei

-

Read more about "Federated Hermes: Weekly Markets Wrap Up 7 May 2026"

Read more about "Federated Hermes: Weekly Markets Wrap Up 7 May 2026"Federated Hermes: Weekly Markets Wrap Up 7 May 2026

-

Read more about "Schroders: Verstoring energievoorziening kan langer aanhouden dan aanvankelijk gedacht"

Read more about "Schroders: Verstoring energievoorziening kan langer aanhouden dan aanvankelijk gedacht"Schroders: Verstoring energievoorziening kan langer aanhouden dan aanvankelijk gedacht

-

Read more about "BNP Paribas: Q1 Global Outlook"

Read more about "BNP Paribas: Q1 Global Outlook"BNP Paribas: Q1 Global Outlook

-

Read more about "RBC BlueBay: Huidige marktdynamiek doet denken aan begin coronacrisis"

Read more about "RBC BlueBay: Huidige marktdynamiek doet denken aan begin coronacrisis"RBC BlueBay: Huidige marktdynamiek doet denken aan begin coronacrisis

-

Read more about "Principal AM: Verbeterend sentiment ondersteunt de kracht van de markt"

Principal AM: Verbeterend sentiment ondersteunt de kracht van de markt

-

Read more about "Payden & Rygel: Economics Forecast"

Read more about "Payden & Rygel: Economics Forecast"Payden & Rygel: Economics Forecast