Harry Geels: Where to emigrate for tax purposes after Box 3 plans?

")

This column was originally written in Dutch. This is an English translation.

By Harry Geels

The adoption of the new Box 3 tax, which also taxes unrealised gains on shares, has caused considerable outrage. More and more Dutch citizens are considering (tax) emigration. In addition to the usual suspects such as Switzerland and the United Arab Emirates, there are also three attractive countries within the EU.

At the end of January, I wrote a column about the then outgoing cabinet's plans to introduce a new Box 3 tax, listing a whole range of arguments against doing so. The biggest objection is that unrealised returns will also be taxed. This undermines the compounding effect of investing and could lead to bizarre situations in which investors pay more tax than they earn in returns. Nevertheless, the new cabinet is also pushing ahead with these plans.

There is no need to repeat all the arguments against capital gains tax. In short, it is an inefficient tax. It costs the Netherlands more than it generates. The costs are, on the one hand, the highly complex collection and possible legal proceedings and, on the other hand, tax avoidance by wealthy individuals. This avoidance takes roughly two forms: tax optimisation (transferring money from Box 3 to Boxes 1 and 2) and tax emigration.

Prediction: tax revenues from new Box 3 will be disappointing

Norway and the United Kingdom show that new wealth taxes lead to further tax optimisation.

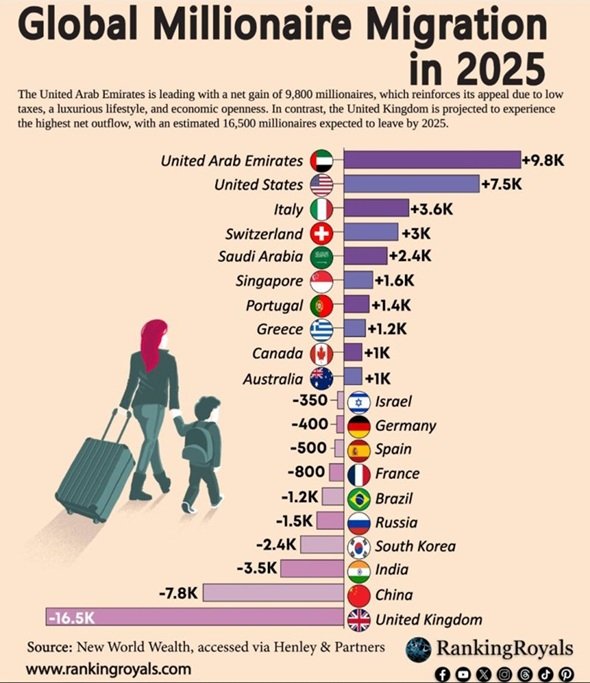

In Norway, the increase in wealth tax led to a significant capital flight: individuals with a combined wealth of 54 billion dollars left the country, resulting in 594 million dollars less in annual tax revenue, whereas the measure was supposed to generate an additional 146 million dollars. Currently, 105 of the 400 wealthiest Norwegians reside abroad.

A similar dynamic played out in the United Kingdom. The abolition of the non-dom regime caused an exodus of 10,800 millionaires in a single year, making the country the world's largest net loss of wealthy residents in 2025. According to Henley & Partners, this is one of the reasons why London has fallen in the ranking of global wealth hubs. Incidentally, the aforementioned forecast of 16,500 departing millionaires (see below) turned out to be an overestimate.

Italy

Switzerland, Andorra, Liechtenstein, Malta, Monaco and the United Arab Emirates (and some even more exotic locations) in particular offer wealthy individuals attractive tax regimes. However, the major problem with these countries is that the cost of living is high. Buying or renting property alone is at least twice as expensive as in the Netherlands. Malta is still somewhat affordable, however. Moreover, social and political integration is difficult there. There are other interesting alternatives, even within the EU: Italy, Portugal and Greece.

Italy has a so-called flat tax on foreign income, originally €100,000 per year and increased to €200,000 since 2024. This makes it possible for wealthy newcomers to buy off all their foreign income at a fixed, low annual rate, regardless of the size of their global assets. This regime can be used for up to fifteen years and can also be extended to family members for a fixed amount.

There is a tax on capital gains and income, but this is lower than what the Netherlands is currently proposing – namely 26% – and only applies to realised gains and income.

Italy is therefore seeing a growing influx of high-net-worth individuals, including entrepreneurs, investors and sports icons. This is a deliberate strategy: by attracting foreign capital flows, the country aims to bring in both capital and talent.

Portugal

Over the past decade, Portugal has developed into a fiscally attractive destination in Europe, initially thanks to the NHR regime and, since 2024, through its successor IFICI (NHR 2.0). This new regime specifically targets highly qualified professionals in science, innovation and technology. It offers a 20% flat rate on Portuguese professional income plus generous exemptions on foreign income, such as dividends, interest, royalties and foreign employment income.

Under the new IFICI regime, virtually all foreign investment income for a Dutch immigrant in Portugal is completely untaxed. The regime acts as an economic catalyst: by attracting talent working in exporting or innovative sectors, Portugal aims to add value to its economy. As a result, despite stricter conditions, the country remains one of the most strategically deployed tax incentives in Europe.

Greece

For several years now, Greece has been explicitly targeting wealthy expats, pensioners and internationally mobile capital with striking tax arrangements. For example, the country offers a flat tax of €100,000 for high-net-worth individuals on all their foreign income, both from employment and capital, for a maximum of 15 years, and a 7% tax rate for foreign pensioners who move their tax residence to Greece.

In addition, the government has announced broad tax cuts for 2026, including lower tax brackets and regional discounts on property and VAT levies. This makes Greece an attractive destination for people with internationally mobile assets.

Joint appeal: climate, costs & lifestyle

What Italy, Portugal and Greece have in common goes beyond tax incentives. All three offer good healthcare, rich culture and nature, a pleasant Mediterranean climate, relatively low cost of living (especially outside the major cities). In short, a quality of life that many Northern Europeans perceive as significantly higher. Their relatively good economic performance in recent years is partly due to the influx of people and capital.

In conclusion: the proposed exit tax

Italy, Portugal and Greece not only offer predictable and internationally competitive tax regimes, but do so within the framework of the European free movement of persons and capital, fundamental rights that are intended to enable precisely this kind of mobility. It is therefore difficult to justify the Netherlands imposing an additional departure tax on wealthy emigrants to these EU countries, as explored in the letters to parliament about a possible additional tax assessment.

Such an exit tax would be both economically counterproductive and legally at odds with the EU right to free movement. Moreover, it would primarily convey the message that the Netherlands is increasingly distrustful of its own wealthy residents. Perhaps it would be wiser to first put its own fiscal house in order, so that Dutch citizens do not have to move to other countries simply to be taxed fairly and predictably.

This article contains the personal opinion of Harry Geels