NN IP: Prospects of an early taper push US yields higher

NN IP: Prospects of an early taper push US yields higher

Financial markets offered investors plenty to mull over in the past week. A strong US jobs report triggered a sell-off in Treasuries, while the ongoing pandemic continues to raise questions about growth prospects and monetary policy. With sentiment towards stocks still strong and corporate earnings impressive, we moved slightly overweight in equities and underweight in US Treasuries.

In a week in which the relative summer calm persisted in the financial markets, three themes dominated. First, stronger-than-expected US non-farm payrolls for July may help bring forward the Fed’s tapering announcement. Second, the spread of the Delta coronavirus variant in China has triggered new travel restrictions and is causing new concerns about global growth. And third, the publication of the United Nations’ Intergovernmental Panel on Climate Change (IPCC) report is likely to increase the pressure on governments to take more radical action to stop global warming.

While the prospects for US monetary policy and global growth will to a large extent determine the performance of financial assets in the short and medium term, we believe that investors with a longer horizon should increasingly take into account the uncertainty and potential economic disruptions resulting from the global climate crisis.

US yields rise on expectations of tapering

US and Eurozone bond yields had been falling in recent weeks due to softer-than-expected growth data, increasing uncertainty about growth and the strong dovish stances of both the Fed and the ECB. Last week, however, interest rate expectations started to rise again after hawkish comments from Fed governors Richard Clarida and Christopher Waller and a solid US jobs report.

The 15bps rise in the US 10-year yield over the past few days is its sharpest increase since April. With 943,000 new jobs, US employment growth was strong in July, even after adjusting for seasonal factors. And with the unemployment rate falling to 5.4% – well below the 5.7% consensus forecast – labour force participation also improved. These figures, in combination with broadening wage pressures over recent months, suggest that the Fed might not be far from announcing the first reduction of its asset purchases.

For now, we still expect a first announcement sometime in Q4, but the risk of earlier measures seems to be rising. The Fed has made it clear that strong jobs figures would be crucial evidence of the “substantial further progress” towards maximum employment that it sees as a prerequisite for policy tapering. At the same time, recent increases in coronavirus infections in states where only around 40% of the population has been vaccinated could hamper the economic recovery and revive the forces of secular stagnation. In such an uncertain environment, the Fed might prefer to change its policy stance later rather than earlier.

The pandemic lingers on

The Delta variant is spreading almost everywhere. Less than 40% of the population have been vaccinated in most emerging countries and even parts of the US. A lack of vaccines, poor health infrastructures and the use of less-effective vaccines are reasons why the number of infections continues to rise in large parts of Asia, the Middle East, Africa and Latin America. Currently, coronavirus is creating most problems in east Asia: the rate of new infections continues to accelerate in South Korea, Thailand and Malaysia. New mobility restrictions are being introduced in the Philippines and manufacturing production is being affected in Vietnam.

Even in China, where health controls have remained very tight since the first outbreak in Wuhan, the virus has been spreading since infected people entered the country from Russia and Myanmar. The numbers are still relatively low, with daily infections below 100. Still, very few Chinese people have been exposed to the virus so far and Chinese vaccines provide only limited protection, so the risk of a serious second wave of infections is not insignificant. As a result, several economists have already started to downgrade their growth expectations for the Chinese economy.

We think it is still too early to draw dramatic conclusions. The Chinese authorities have a good track record in containing the virus and the numbers of new infections in Nanjing and Zhengzhou, where the current Delta breakout started, have already started to come down. What’s more, the government has instigated a new round of economic policy stimulus in the past few weeks.

We expect construction growth to start accelerating before the end of the year. Meanwhile, however, new travel restrictions have already resulted in sharply lower seat occupancy (down 32% over the past week) in Chinese airplanes, and this is likely to start having an impact on services expenditure growth. We expect the Chinese economy to grow by 9.0% this year and by 5.5% in 2022.

We move overweight in equities, underweight in US Treasuries

We made two changes to our multi-asset portfolio: we re-opened a moderate overweight in equities and a moderate underweight in US Treasuries. Despite these changes, the portfolio is still adopting a relatively low risk profile. It remains moderately overweight in Eurozone high-yield credit and crude oil.

We increased our exposure to equities primarily because sentiment indicators remained resilient despite the modest softening in macroeconomic data. Our medium-term quant signals are also favourable for stocks. From a fundamental perspective, we continue to be impressed by strong corporate earnings momentum: with earnings estimates still being upgraded, the earnings upgrade/downgrade ratio remains positive across all regions. This means the equity risk premium should still have room to tighten.

Ten-year US Treasury yields have risen for five days in a row, while expectations of Fed tapering have increased since the July jobs report. Market participants are also adjusting their rate hike expectations; the first hike is now priced in for Q1 2023. Positive labour market dynamics should gradually increase the market’s confidence in a more hawkish Fed.

With expectations of tapering rising, the term premium should increase, pushing 10-year yields higher. This is the main reason we moved underweight in US Treasuries. We are keeping a close eye on the Delta variant in the US, which is the main risk for growth expectations in the short term. Adverse developments could keep the Fed on hold for longer than we currently anticipate.

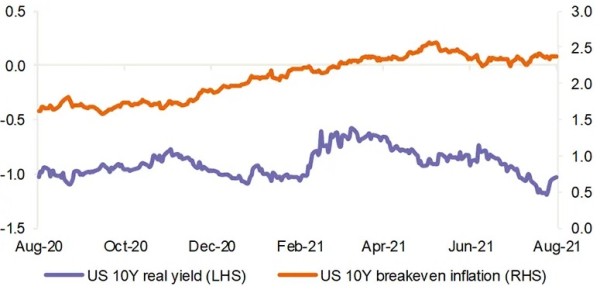

Decomposition of US 10-year nominal bond yield

%, real yield and breakeven inflation Source: Bloomberg

Precious metals and energy have fallen sharply in the past week. The rise in US real yields (see figure), the appreciating US dollar and the Delta variant are clearly weighing on investment demand for broad commodities. The spread of the Delta variant has increased concerns about a fall in demand for energy, but with global growth momentum holding up reasonably well – the global composite PMI hit 55.7 in July – we think these concerns are slightly overdone.

Demand from Chinese refineries is expected to pick up again after maintenance of refinery facilities had pushed it lower. We remain overweight in US WTI crude as we expect further declines in oil inventories. Moreover, the return of Iranian oil to the market is likely to be postponed given the increasing tensions between the new Iranian government and the US.

Share this post!

Related posts

-

Read more about "Harry Geels: Trump's call to lower interest rates is grotesque and dangerous"

Read more about "Harry Geels: Trump's call to lower interest rates is grotesque and dangerous"Harry Geels: Trump's call to lower interest rates is grotesque and dangerous

-

Read more about "Ethenea: How monetary policy independence is being eroded"

Read more about "Ethenea: How monetary policy independence is being eroded"Ethenea: How monetary policy independence is being eroded

-

Read more about "Payden & Rygel: Is the US going broke?"

Read more about "Payden & Rygel: Is the US going broke?"Payden & Rygel: Is the US going broke?

-

Read more about "Swissquote: BoE’s got the greenlight"

Read more about "Swissquote: BoE’s got the greenlight"Swissquote: BoE’s got the greenlight

-

Read more about "AllianzGI: Japanse renteverhoging verwacht"

Read more about "AllianzGI: Japanse renteverhoging verwacht"AllianzGI: Japanse renteverhoging verwacht

-

Read more about "Aberdeen: All ingredients for further interest rate cuts by the BoE are there"

Read more about "Aberdeen: All ingredients for further interest rate cuts by the BoE are there"Aberdeen: All ingredients for further interest rate cuts by the BoE are there

-

Read more about "Fidelity: Beleggers moeten posities in VS verkleinen vanwege AI-hype"

Read more about "Fidelity: Beleggers moeten posities in VS verkleinen vanwege AI-hype"Fidelity: Beleggers moeten posities in VS verkleinen vanwege AI-hype

-

Read more about "Schroders: Amerikaanse aandelenmarkten blijven de toon zetten"

Read more about "Schroders: Amerikaanse aandelenmarkten blijven de toon zetten"Schroders: Amerikaanse aandelenmarkten blijven de toon zetten

-

Read more about "MFS: Amerikaanse midcap bedrijven zullen goed presteren in 2026"

Read more about "MFS: Amerikaanse midcap bedrijven zullen goed presteren in 2026"MFS: Amerikaanse midcap bedrijven zullen goed presteren in 2026

-

Read more about "J. Safra Sarasin: IG EMD goed alternatief voor Amerikaanse bedrijfsobligaties"

Read more about "J. Safra Sarasin: IG EMD goed alternatief voor Amerikaanse bedrijfsobligaties"J. Safra Sarasin: IG EMD goed alternatief voor Amerikaanse bedrijfsobligaties