Fidelity: Risk averse income seekers need look no further than sterling investment grade

Fidelity: Risk averse income seekers need look no further than sterling investment grade

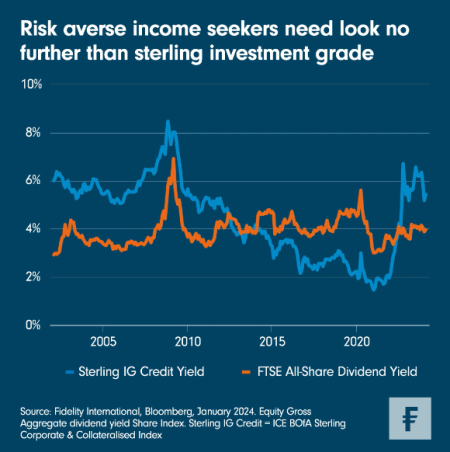

Yields on investment grade corporate debt look attractive after a difficult period for fixed income. This is useful at a time when it makes sense to act defensively.

Bond investors can now find a decent income from the relative security of sterling investment grade (IG) credit. After two years of tightening monetary policy, IG offers yields that sit well above benchmark gilts (107 basis points) and, for the first time in a decade, the UK’s famous dividend payers. This week’s Chart Room shows the yield available on sterling IG credit stands around 100bps higher than that on the FTSE All-Share index.

The renaissance in sterling IG credit comes at a time when there is an argument for shoring up a portfolio’s defences. High-quality issuers will have a prominent role to play as the effect of monetary policy tightening starts to feed through to the economy. Increased borrowing rates have seen insolvencies rise by 10 per cent year-on-year, highlighting the risks to lower-rated corporates and their bonds.

But it’s not just about credit quality: duration, or interest rate risk, is another important consideration. Today’s inverted yield curve means the income available on shorter-dated credit can be higher than that at the longer-end of the curve, which itself comes with higher duration and credit risk.

Moreover, shorter-dated credit has a higher sensitivity to near-term interest rates. We have seen before (most recently in 2008) how a rapid slash in rates has led to a rally in short-term bonds, and a steepening of the spread between short and long-dated yields. Locking in those yields now brings with it the prospect of decent capital return if and when rates do eventually fall.

The downside? Well, missing out on higher yielding (but riskier) credit, especially if the Bank of England continues to keep rates high. But we think that’s unlikely, and that recession risk looms large. Shorter-dated IG offers relative security in the event of a downturn, with decent yields that mean investors need not miss out on returns.

There are attractive sectors within this world that can add further protection - utilities, for instance, are inflation-protected and defensive in nature. In contrast, cyclicals and banks look risky for the time being. The bottom line: taking a more defensive approach now need not mean investors are forced to give up on yield.

Deel dit bericht

Gerelateerde berichten

-

Lees meer over "DPAM: Outlook 2026 bedrijfsobligaties"

Lees meer over "DPAM: Outlook 2026 bedrijfsobligaties"DPAM: Outlook 2026 bedrijfsobligaties

-

Lees meer over "Payden & Rygel: Macro Outlook Investment Grade Credit"

Lees meer over "Payden & Rygel: Macro Outlook Investment Grade Credit"Payden & Rygel: Macro Outlook Investment Grade Credit

-

Lees meer over "BlackRock: Barsten in het concept van portefeuillediversificatie"

Lees meer over "BlackRock: Barsten in het concept van portefeuillediversificatie"BlackRock: Barsten in het concept van portefeuillediversificatie

-

Lees meer over "Ossiam: Stijgende overheidsschulden bedreigen bedrijfsinvesteringen"

Lees meer over "Ossiam: Stijgende overheidsschulden bedreigen bedrijfsinvesteringen"Ossiam: Stijgende overheidsschulden bedreigen bedrijfsinvesteringen

-

Lees meer over "Janus Henderson: Obligaties profiteren van lager renteklimaat"

Lees meer over "Janus Henderson: Obligaties profiteren van lager renteklimaat"Janus Henderson: Obligaties profiteren van lager renteklimaat

-

Lees meer over "Crédit Mutuel AM: Fixed income convictions"

Crédit Mutuel AM: Fixed income convictions

-

Lees meer over "DWS: Nederlandse pensioenfondsen drukken stempel op Europese obligatiemarkt"

Lees meer over "DWS: Nederlandse pensioenfondsen drukken stempel op Europese obligatiemarkt"DWS: Nederlandse pensioenfondsen drukken stempel op Europese obligatiemarkt

-

Lees meer over "Crédit Mutuel AM: Monthly commentary on subordinated debt"

Crédit Mutuel AM: Monthly commentary on subordinated debt

-

Lees meer over "Rendement en impact bij duurzaam gelabelde obligaties (Ronde Tafel 'Green, Blue & Orange Bonds' – deel 2)"

Lees meer over "Rendement en impact bij duurzaam gelabelde obligaties (Ronde Tafel 'Green, Blue & Orange Bonds' – deel 2)"Rendement en impact bij duurzaam gelabelde obligaties (Ronde Tafel 'Green, Blue & Orange Bonds' – deel 2)

-

Lees meer over "J. Safra Sarasin: IG EMD goed alternatief voor Amerikaanse bedrijfsobligaties"

Lees meer over "J. Safra Sarasin: IG EMD goed alternatief voor Amerikaanse bedrijfsobligaties"J. Safra Sarasin: IG EMD goed alternatief voor Amerikaanse bedrijfsobligaties