Harry Geels: The seven lessons of a hundred inflation shocks

By Harry Geels

Economists from the IMF examined more than 100 inflation episodes in different countries. This yielded several instructive lessons, for example that inflation is persistent, that the fight against inflation almost always cheers too early, and that the key to fighting inflation is strict monetary policy.

In the Netherlands, inflation in August amounted to 3% (in July it was still 4.6%). Excluding energy, the inflation rate last month was 6.4%. This means that inflation is falling but still too high. Last Thursday, Christine Lagarde spoke remarkably stern words when announcing the tenth interest rate increase to 4% on September 20. The ECB will do what is necessary to help inflation to 2%. Governments must help by reducing debts and stopping all kinds of support for companies.

I have sometimes been critical of the ECB's policy, but Lagarde's words now sounded like music to my ears. The previous criticism concerned the negative interest rate that should never have been introduced (because it would increase the debt mountain) and starting to raise interest rates too late (believing in a fairy tale of temporary inflation). In the context of the current fight against inflation, it is interesting to take note of a recently published working paper by economists from the IMF about the lessons that can be learned by studying more than 100 inflation shocks.

The IMF study covered the period from 1973 to the present and covered 56 countries. Let's first discuss the seven lessons – the research refers to 'stylized facts'. We then conclude with some general comments about inflation and the current fight against it.

1) Inflation tends to be persistent (especially after trade shocks)

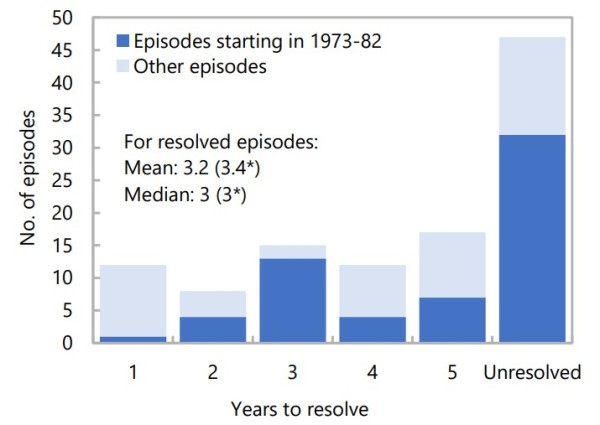

Figure 1 shows that the vast majority of inflation shocks only resolve after years. In the majority of cases even after more than five years. When it comes to trade shocks, such as the oil crisis in the 1970s, fighting inflation usually takes longer. Most of the cases where inflation came back under control within a year involved financial shocks (particularly the credit crisis of 2008-2009 and the Asian crisis of 1997). Then, economically speaking, short hard landings quickly occurred, bringing inflation back to a standstill.

Figure 1: Years until inflation falls to within 1% of the pre-shock rate

Footnote: *Episodes starting 1973–82; source: IMF staff calculations.

2) Most of the unresolved inflation episodes involved 'premature celebrations'.

In about 90% of the unresolved periods (42 out of 47 in the full sample and 28 out of 32 during the 1973-1979 oil crises), inflation fell significantly within the first three years after the initial shock but then stagnated at a high level or accelerated it again. Various explanations are given in the study, such as policy easing too quickly when inflation started to fall again, or simply pure base effects (inflation is still rising, but less rapidly because the factors behind the initial inflation shock decrease).

3) Countries that solved inflation had tighter monetary policies

Countries that successfully tackled inflation had higher real interest rates (which were positive on average, in contrast to unsuccessful countries that had negative real interest rates), negative money supply growth, and limited deviation from the Taylor Rule. Furthermore, countries that brought inflation under control earlier had inflation better anchored. That is, economic conditions had little impact on long-term inflation. There are short-term effects, but they offset each other in the longer term.

4) Countries that resolved inflation adopted more consistently restrictive policies

Consistent monetary policy, defined in terms of fluctuations in monetary instruments such as interest rates and money supply, also helps. The more consistent the policy, i.e. the less volatility in interest rates and money supply growth, the better.

5) Countries that resolved inflation kept nominal exchange rate depreciation in check

A stable currency, for example not abandoning a link to a strong currency, turned out to be a better policy. A stronger currency keeps the negative effects of import inflation under control. The trade balance was comparably negative for both groups of countries.

6) Countries that resolved inflation had lower nominal wage growth

Although the statistics are not as robust as the other lessons, keeping nominal wage growth in check appears to help fight inflation. The 'successful' countries examined in the sample even show negative nominal wage growth.

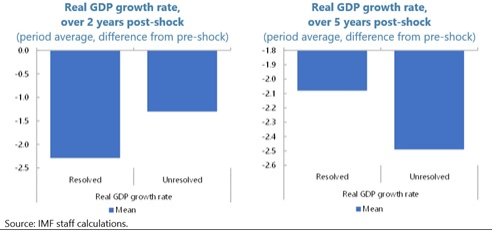

7) Countries that resolved inflation had lower growth in the short term, but not over a 5-year horizon

Effectively, combating inflation temporarily leads to negative economic growth. The IMF economists conclude: “successful disinflations pay off in the medium term because they avoid the costs of persistently high inflation, including macroeconomic instability.”

Figure 2: GDP growth over 2 and 5 years (countries that do and do not fight inflation well)

Some final comments on inflation policy

Inflation is not a good thing. It destroys purchasing power and harms lower income groups more than higher income groups because they spend a greater share of their income. Ernest Hemingway once wrote an appropriate quote: 'The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin. But both are the refuge of political and economic opportunists.' A 2% inflation target is actually too high. In any case, inflation is difficult to manage precisely; a zone of 0-2% would be more realistic.

Interestingly, the researchers also found that countries that controlled inflation more quickly had policy rates that deviated less from the Taylor Rule than less successful countries. According to Emeritus Professor Sylvester Eijffinger, the policy interest rate based on the Taylor Rule should now be around 4.5%, so still 0.5 percentage points above the current monetary rate. He rightly states that second and third rounds of inflation effects are still to come. Moreover, with a Taylor Rule, or with another algorithm (for example neutral interest rate +0.25%), monetary policy can be made very objective, simple and predictable.

It is striking in the IMF study that oil in particular (the first oil crisis in 1973 and the second in 1979) causes inflation, together with food. It is therefore strange that core inflation excludes precisely these two components. Food and energy are basic needs. As far as I'm concerned, the real inflation for August was 6.4%. Furthermore, central banks have little influence on energy and food prices. We can push the economy into a recession, but that does not mean that energy and food prices will fall.

This article contains a personal opinion from Harry Geels