Columbia Threadneedle: Which way next?

Please find below Columbia Threadneedle’s latest Asset Allocation Update, by Maya Bhandari, Multi-Asset Portfolio Manager. Maya looks at how our outlook has changed since the start of 2019, how investors are wary of being either too optimistic or pessimistic, and at Asia’s quiet but steady recovery.

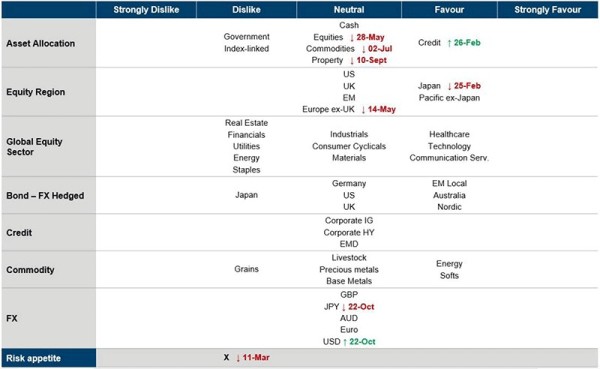

As 2019 draws to a close, we are strikingly neutral across asset classes and with considerably less appetite for risk than at the start of the year (Figure 1). Various market positioning and flow measures suggest we are in good company: notwithstanding punchy headline year-to-date returns from several markets, the investor community in toto is cautiously positioned and on many measures has turned increasingly so over the course of the year. In just the past fortnight, company earnings beats have been handsomely rewarded, with misses only gently punished, if at all. Folk are nervous about being caught too optimistic, or too pessimistic. So what would we look to today, to turn less neutral?

Figure 1: Striking neutrality

Source: Columbia Threadneedle Investments, 4 November 2019.

Four key factors

Four developments would tip the scales away from broad neutrality, two in each direction. Evidence that manufacturing malaise is spreading to the consumer and/or under-delivery of anticipated easing by global central banks would augur greater caution. Conversely, a deceleration in geopolitical tensions (chiefly trade and Brexit) and/or more evidence that the rise in Asian PMIs is crystallising and spreading to other regions would inspire greater confidence.

The problem is that these four forces are actively pulling in different directions. Take the last week of October. While the strength of consumption in US GDP (and elsewhere, such as France and Japan) was reassuring, investment has contracted in three of the past six quarters in the US and leading indicators point to more weakness in the offing.

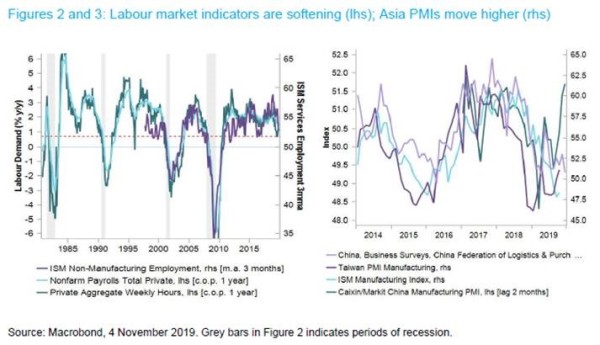

Although major countries tend to be dominated by consumer spending, post-war recessions in most developed economies uniformly coincide with falls in (typically volatile) investment and inventories1. The statistical relationship between investment and consumption is not particularly strong, but consumption has done most of the heavy lifting for growth in recent quarters. And several indicators of labour demand have weakened to the lower end of the post-global financial crisis range: although still too firm for recession, deceleration is both palpable and as expected at this stage in the cycle (Figure 2).

The US Federal Reserve, meanwhile, hinted at being closer to the end of its insurance easing cycle than markets (continue to) anticipate. Insofar as this cycle was designed to deliver a swift 75 basis points of easing akin to the 1990s (and pause absent further trade war escalation/economic weakness), the Fed’s pivot might be complete – although the outcome on trade is not yet certain, as discussed below.

On balance, however, the risks appear asymmetric: with two more interest rate cuts priced in from the Fed next year, and one more from both the BoE and ECB (with rates expected to then stay below inflation for the next 10 years), under-delivery right now would be a bigger surprise. It is also worth noting that the next round of proposed tariffs are consumer product-focused, and may be more problematic for the Fed’s inflation target than recent rounds where growth concerns dominated.

Brexit and trade

The direction of travel on both global trade and Brexit has been favourable recently – on Brexit, because the prospect of a hard/accidental Brexit has been removed in the immediate term with a UK general election due in early December, and on trade following progress on “phase one” of US-China negotiations. Ultimate destinations, however, remain far from clear. In the UK, odds are 50:50 for a hung parliament, meaning all Brexit options are still effectively on the table. The current trade truce for the US and China, meanwhile, also lapses in early December, when a decision on future tariffs is also due. No progress has been made on thornier issues of intellectual property, for example.

Yet quietly, amid the noise, Asia has been steadily recovering with Taiwanese and Chinese PMIs, for example, at multi-month highs (Figure 3). One striking side effect of the trade war in Asia has been the internalisation of supply chains: companies such as Huawei have built up to two years of supply chains, all sourced within Asia; similar stories abound across 5G companies. Semi-conductors, one of the most sensitive sectors to both cyclicality and trade, have recovered sharply in both asset prices (eg, the PHLX Semiconductor Sector Index, known as the SOX) and volumes (new orders) as an Asian mini-cycle takes hold. Recent data from Europe, Japan and most recently the US add to this mosaic of stability.

Whisper it: Asia is recovering ahead of the rest, and at least one aspect of the trade war might make the region less exposed to the vagaries of the global cycle.

Our asset allocation views have not changed and greater caution versus, say, a year ago remains prudent at the current juncture. But as the dust settles, we have been nibbling into greater Asian equity exposure.

1 Treading a more tenuous path, Asset Allocation Update August/September 2019, Columbia Threadneedle Investments.