State Street SPDR ETFs: Short duration emerging markets hard currency

The Federal Reserve (Fed) is sticking to its projection of three rate cuts starting in June. There had been some speculation in the market of a shift to signalling just two cuts this year, but higher growth and inflation projections have not yet proved sufficient to tip consensus on the FOMC towards a more moderate easing path — although one cut was removed from the dot-plot profile in 2025.

The backdrop created by the rather sticky path for inflation and the seemingly continual upgrades to growth has been tricky for fixed income investors to navigate. Short duration, risk-on strategies have been the best performing year to date mainly because the mechanics of a high coupon coupled with a shorter duration creates a very defensive profile. For these types of strategies, yields have to rise to a significant degree for there to be losses.

The economic backdrop has also supported the US dollar, and the US Dollar Index (DXY) remains around 2.5% higher than it was at the end of 2023. Despite being more positive for risk assets generally, this USD strength has weighed on the performance of emerging market (EM) local currency debt. The same headwinds have not been felt in hard currency exposures, which have performed better year to date, driven by coupon interest and spread returns as credit spreads compress.

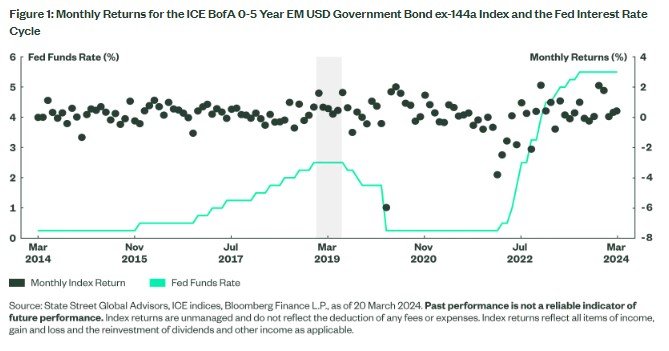

The history of the 2016-2019 Fed tightening cycle hints at the benefits of short duration emerging market hard currency exposures. Figure 1 illustrates that monthly returns for the ICE BofA 0-5 Year EM USD Government Bond ex-144a Index (the dots) remained positive when rates in the US were at their peak. It has been a similar story for the current cycle; since rates peaked in July 2023, only two of the nine months since then have suffered negative returns.

The performance drivers are clear: Yields are high, both because underlying US Treasury yields are at the top of the cycle and because EM debt enjoys a spread. The US dollar typically remains quite well supported given the yield advantage often enjoyed at the top of the cycle. A strong US economy is generally a positive for global growth and, therefore, risk assets. With respect to emerging markets, it should reduce fears over a general deterioration in country ratings.

While seasonal factors are likely to prove less of a driving factor than Fed policy, Q1 is typically the trickiest period for returns. April and May have had negative returns just twice each over the past 10 years.

Jason Simpson, Senior Fixed Income Strategist at State Street SPDR ETFs:

'Investors generally accept that there are always idiosyncratic risks in EM exposures but given the broad diversification of hard currency, this is typically less of a concern. It is the bigger macro drivers that are more important and, as can be seen in Figure 1, once the Fed actually starts to deliver its rate cuts the path for hard currency becomes more nuanced.

In the 2019-2020 cut cycle there were several instances of negative monthly returns before Covid saw a wider market aversion to risk. While US Treasuries rallied into 2020, supporting returns, EM credit spreads widened as expectations of slower global growth increased. With spreads currently at historically tight levels, close to the lows seen in 2018, this is a potential risk. However, the higher yields on offer in 2024 do provide investors with some protection.

Dividing the index yield to maturity by its duration gives an indication of the degree to which yields will need to rise in order for the strategy to start losing money. In the case of the ICE BofA 0-5 Year EM USD Government Bond ex-144a Index, it is over 260 basis points. While yield moves in EM can be significant, this implies either an upturn in US inflation (forcing another round of Fed tightening) or a big risk-off event resulting in a spread blow-out.'