Harry Geels: Investing to maintain purchasing power

Harry Geels: Investing to maintain purchasing power

This column was originally written in Dutch. This is an English translation.

By Harry Geels

Although inflation figures are coming down again, it is an illusion to think that we will have low inflation in the long term. There is therefore no other option than to invest, especially in shares.

Inflation is on a downward trend, but remains firmly above 2%. In February, the Netherlands registered a consumer price level that was 2.8% higher than a year earlier. The euro area as a whole had an inflation rate of 2.6%, slightly lower. These figures are a disappointment, especially because the level being compared already represents a sharply increased price level from the previous year.

There is a chance that inflation will fall further in the short term, but in the longer term there are plenty of reasons to take higher inflation into account. Let's list the reasons for slightly higher inflation in the coming years, and then answer the important question of how to deal with this as an investor.

Reasons why inflation remains (relatively high).

Inflation is a many-headed dragon. The fact that central banks think that they can keep this under control with policy is a gross overestimation. There are at least ten dark inflationary forces that can be named. In fact, simple forms of monetary policy are sufficient, such as growing the money supply with economic growth, a 'neutral interest rate', or using another benchmark such as the Taylor Rule. But central alchemists prefer to stir a mysterious monetary soup, while pursuing other (political) goals.

There are several reasons why we have entered an era of higher inflation on average, although inflation targets of an average of 2% per year may be accidentally achieved. The main reason is that there is a record amount of debt outstanding worldwide. For consumers, for companies, but especially for governments, with the biggest fear being the US national debt that is now growing by $1 trillion per hundred days. A lot of inflation is needed to keep it within acceptable ratios. Inflation is a bailout for debtors.

The second reason is that government debts will continue to increase in most countries. This is due to looser fiscal morality as a result of various major expenditure items, such as the environmental transition and the rearmament of Europe. Third, second and third order effects will follow. Not all entrepreneurs, especially small and medium-sized enterprises, have been able to raise their prices sufficiently to restore their profitability before the wave of inflation. The wage-price spiral has also not yet been worked out. And many megacaps have (too) much pricing power.

Real returns are the right benchmark

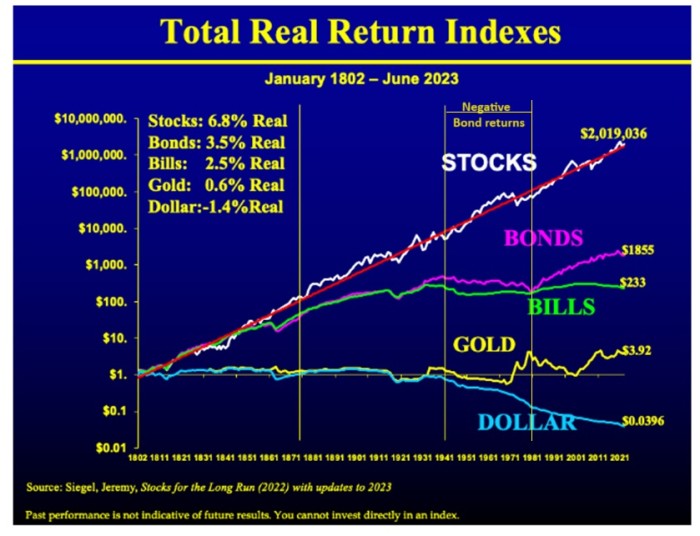

Because (higher) inflation causes the purchasing power of assets to evaporate over time, institutions and wealthy individuals are forced to invest, especially with the (far too low) savings interest rate that banks now offer. A first indication of what to do with the money comes from a study of real returns, especially in long periods of high inflation. According to Figure 1, courtesy of Jeremy Siege, stocks deliver the highest inflation-adjusted returns over the long term.

Figure 1

But Figure 1 contains another important message, namely that bonds (and money market solutions) have a negative trend in times of high inflation. Look at the seventies. We have now entered such a period again since inflation started rising at the end of 2021. Bonds now mainly play a role as a source of diversification and cash flow management. In the near future, they will probably no longer be the guardians of preserving the purchasing power of assets. The same probably applies to gold (and cryptos) as sources of diversification.

Different perspective on inflation compensation

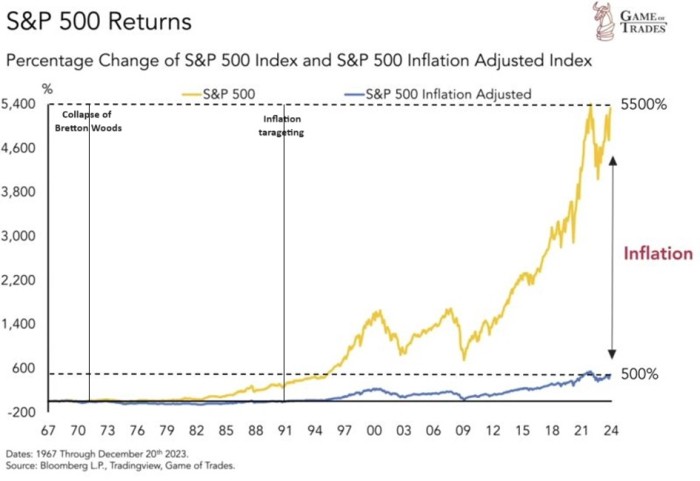

A different perspective on inflation compensation is obtained by comparing the long-term nominal returns of, for example, shares with the real returns. In Figure 2 we see the total return over the period 1967 to 2023 for S&P. The difference is glaringly large. The real return was 500%, nominally 5500%. The difference is the inflation compensation. Theoretically, there is also a good reason why shares are suitable as inflation compensators. Companies that cannot pass on inflation will not last long. They are part of it.

Figure 2

Shares have historically achieved exceptional performance since the early 1980s. Better than most decades before. There are two important reasons for this. Firstly, the monetary policy that has encouraged inflation, first through the dismantling of Bretton Woods in 1971 and since the early 1990s with 'inflation targeting' (and in crises also with supportive policies, also called the 'Greenspan put' ). Secondly, by neoliberalism, which played into the hands of companies with fewer rules and the associated globalization.

Finally, some nuances

Stock markets are very sentiment-driven. Over short periods, inflation compensation is not a foregone conclusion. Crises can temporarily throw a spanner in the works. Stock volatility isn't for everyone. Moreover, history has shown that not all types of shares do well in periods of inflation. Value stocks, for example, tend to outperform growth stocks, although the roles now seem to be reversed. Which again indicates that there are no certainties, except perhaps the 'certainty' that we have to invest to maintain our purchasing power.

This article contains a personal opinion from Harry Geels

Share this post!

Related posts

-

Read more about "Harry Geels: What economists are not telling you about high inflation"

Read more about "Harry Geels: What economists are not telling you about high inflation"Harry Geels: What economists are not telling you about high inflation

-

Read more about "DNB: De gevolgen van overheidsbeleid voor inflatie"

Read more about "DNB: De gevolgen van overheidsbeleid voor inflatie"DNB: De gevolgen van overheidsbeleid voor inflatie

-

Read more about "Harry Geels: Financial repression once again"

Harry Geels: Financial repression once again

-

Read more about "DWS: Inflation up again in December"

Read more about "DWS: Inflation up again in December"DWS: Inflation up again in December

-

Read more about "Doijer & Kalff: Inflatieangst drijft beleggers naar goud"

Read more about "Doijer & Kalff: Inflatieangst drijft beleggers naar goud"Doijer & Kalff: Inflatieangst drijft beleggers naar goud

-

Read more about "Ostrum AM: BoJ zet belangrijke stap naar normalisatie monetair beleid"

Read more about "Ostrum AM: BoJ zet belangrijke stap naar normalisatie monetair beleid"Ostrum AM: BoJ zet belangrijke stap naar normalisatie monetair beleid

-

Read more about "Schroders: Renteverhogingen te snel en te fors ingeprijsd"

Read more about "Schroders: Renteverhogingen te snel en te fors ingeprijsd"Schroders: Renteverhogingen te snel en te fors ingeprijsd

-

Read more about "Swissquote: BoE’s got the greenlight"

Read more about "Swissquote: BoE’s got the greenlight"Swissquote: BoE’s got the greenlight

-

Read more about "Harry Geels: Trump's call to lower interest rates is grotesque and dangerous"

Read more about "Harry Geels: Trump's call to lower interest rates is grotesque and dangerous"Harry Geels: Trump's call to lower interest rates is grotesque and dangerous

-

Read more about "AllianzGI: Japanse renteverhoging verwacht"

AllianzGI: Japanse renteverhoging verwacht