Harry Geels: Monetary policy contributes to social dissatisfaction

This column was originally written in Dutch. This is an English translation.

By Harry Geels

The dissatisfaction with the current political-economic system is due to the 'negative' effects of monetary policy since 1971 rather than to the failure of capitalism. John Maynard Keynes predicted in 1919 that a system will collapse if the value of the currency is compromised.

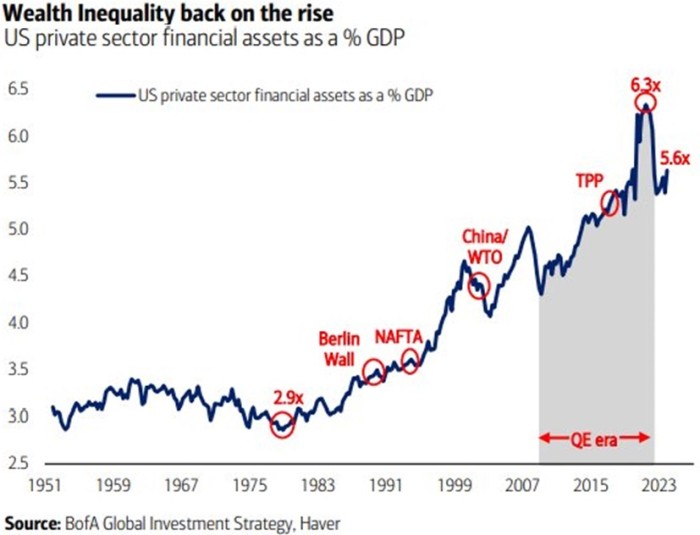

One of BofA Global's latest research reports featured a graph with the telling title 'Wealth Inequality back on the rise'. One of the indicators that the American investment bank uses for this statement is to divide the nominal value of the investments ('assets' in Figure 1) held by the public sector by GDP. In the US, this benchmark has risen to 5.6. In the early 1970s this was still 2.9. Especially during the QE period, the benchmark increased enormously, from 4.3 to 6.3. Printing money ultimately drove up stock prices (and later inflation).

Figure 1

Now the measure 'value of private assets/GDP' does not directly say anything about the distribution of wealth. Nevertheless, BofA speaks of increasing inequality, because other measures show that since the early 1980s, the largest investors have benefited the most: in the US, the richest 10% and especially the very richest 1%. Logically, the more investments someone has, the more they potentially benefit from rising asset prices. Although the above picture concerns the US, a similar picture applies to other large countries such as China, India and Russia. For Europe it is slightly less clear.

Two major monetary policy changes

One of the main causes of the sharp increase in assets was monetary policy. As Figure 1 shows, asset inflation has soared during QE. But monetary policy has actually been the cause of asset inflation before. The first major monetary policy change occurred in 1971, when the Bretton Woods system was dismantled and the US dollar was no longer pegged to a fixed amount of gold. The world's major currencies then began to fluctuate freely (versus the dollar).

This policy has led to increasingly free, expansive monetary policy, partly because dollars no longer had to be exchanged for gold in the US. The second major monetary change came in the early 1980s. After the inflation of the 1970s came under control, central banks were able to lower (policy) interest rates further and further on balance for more than three decades. With every economic crisis, monetary policy became looser by default. Regular interventions were even made in the markets by purchasing assets – the central banks as a helping hand for the investor.

Both changes have made the biggest contributions to rising prices (and growing inequality between the 'haves' and 'have-nots' in the West) in recent decades. Falling interest rates (via the simple discounting of future cash flows) make investments more valuable (on paper) and putting extra money into circulation destroys the value of the currency. The price increases are partly the result of a currency losing purchasing power. The increase in value of a house, for example, partly comes from the depreciation of the currency.

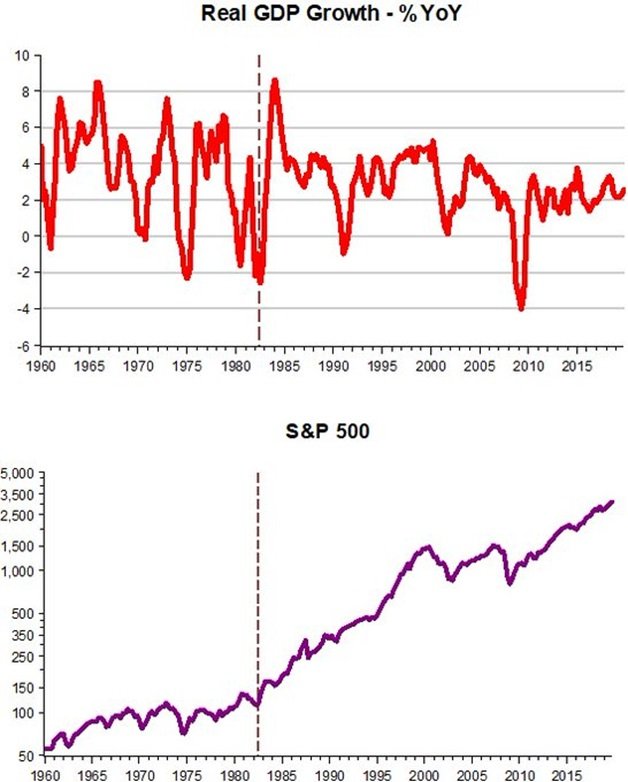

Many people think that economic growth is the main driver behind rising stock prices. This statement is much more difficult to substantiate than the statement that (loose) monetary policy causes prices to rise. For example, Figure 2 shows year-on-year economic growth (top) and the price development of the S&P500 (bottom). While economic growth has become lower on average after the second monetary policy change, prices have nevertheless risen much faster than before.

Figure 2

Keynes already predicted it

One of the greatest economists of all time predicted in 1919 that the capitalist system would be destroyed if the value of the currency were squandered or squandered. In the text below from The Economic Consequences of Peace, John Maynard Keynes warned about the consequences of the Treaty of Versailles. The enormous debts that Germany would have to repay would lead to major inflation and economic-political destruction.

‘Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security but [also] at confidence in the equity of the existing distribution of wealth.

Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become ‘profiteers’, who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat. As the inflation proceeds and the real value of the currency fluctuates wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery.

Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.’

In the text above, Keynes also explains in detail what inflation means: 'impoverishing many while enriching some'. And also: 'those who [supposedly] benefit become the subjects of hatred towards the bourgeoisie', just as is happening again. The question is whether we should blame the rich for getting rich, or criticize the (monetary) system that has facilitated inequality?

The cocktail of monetary, neoliberal and globalist policies

To be clear, the issue of inequality is broader than just monetary policy. The inequality is a cocktail of three developments that took place simultaneously. The neoliberal policies that were embraced from the 1980s onwards (also by the New Left) and globalization have also played a role, with the caveat that both neoliberalism and globalization have also brought much good. At a global level, inequality has declined sharply, because poverty has been sharply reduced, especially in emerging markets.

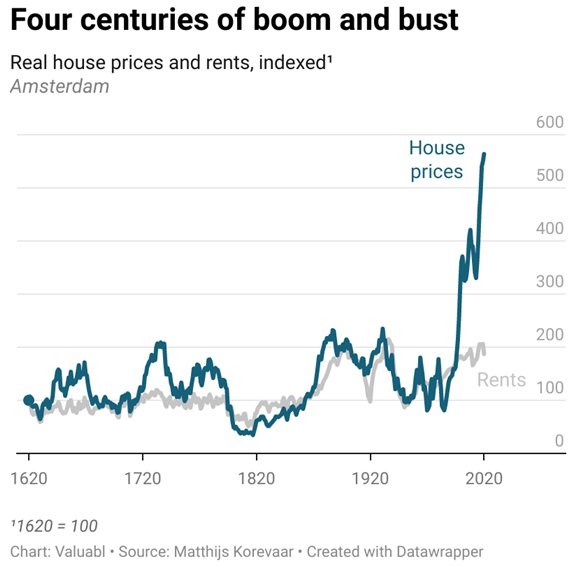

The cocktail of loose monetary, neoliberal and globalist policies was mainly reflected in the major international cities, in addition to the long-standing urbanization and insufficient growth of new housing. Due to globalization, they functioned as magnets for expats. And neoliberalization (partly due to less regulation) made investing in real estate easier. Add to that the increasingly lower interest rates and the tax advantage of debt over equity and voilà, you get historically disproportionate real estate price increases, as we have seen in Amsterdam, but also in many other major cities.

Figure 3

To conclude

It is remarkable that people who denounce inequality mainly focus on neoliberalism (and sometimes also globalism), but much less on monetary policy. Even Thomas Piketty, much praised in left-wing circles, who has done a lot of research into inequality, shows this omission. Whether this is due to a lack of monetary and financial-economic knowledge, or because an institution such as the ECB is de facto a government institution that can intervene 'politically' in the system (and therefore does not encounter objections from people who primarily believe in the government instead of the market) I can't fully fathom yet.

The above story shows that we must invest, because investments are more stable in the long term than the currency.

This article contains a personal opinion from Harry Geels