Harry Geels: Europe is lagging record behind the US

")

By Harry Geels

European stock markets recently reached a record low in terms of valuation compared to the US. That is a painful conclusion, all the more so because there is quite a lot to criticize about the US. There are roughly seven reasons for the European default. The question is whether the tide can turn in favor of Europe.

Like no other literary book, Grand Hotel Europa by Ilja Leonard Pfeijffer paints a disconcerting picture of Europe, an old continent that is only crushed by mass tourism (something that, paradoxically, given its polluting nature, does not suit Europe's climate agenda at all). 'Old Europe' lags far behind the US when it comes to economic indicators, including stock market performance and economic growth.

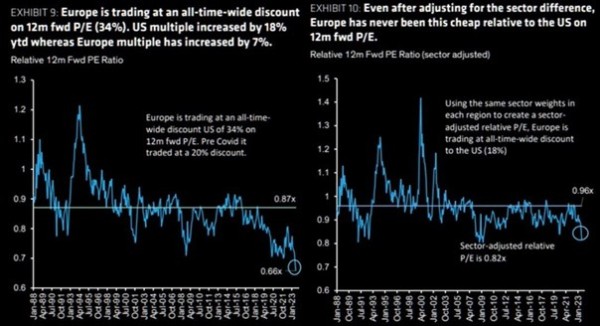

At the end of June, European equities reached a record valuation deficit. Based on the forward p/e ratio, they are 34% cheaper than US equities. Even after adjusting for sector differences (in the US, the technology sector is much more dominant than in Europe), a record difference in valuation remains, even though the valuation of European equities is 18% lower. This year the price-to-earnings ratio in the US increased by 18% versus 7% in Europe. There are roughly seven explanations for this much better performance of US equities.

Figure 1: European equities have never been so cheap compared to US equities

Source: AB Bernstein

1) More liquid markets

The first explanation for the higher valuation of US equities is the better liquidity on the stock exchanges. There is much more efficient and deeper trading. In general, the easier shares are to trade, the more expensive they become. Investors are willing to pay a premium for the ease of entry and exit. As a result, larger stocks tend to be more expensive in terms of fundamental ratios than smaller stocks. Liquidity is also referred to as a 'virtuous circle': it attracts, among other things, IPOs and new liquidity.

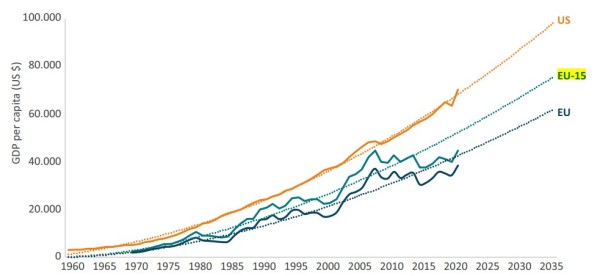

2) Higher economic growth

The US economy has been growing faster than that of the EU for many years. There are several explanations for this, but the most important are higher population growth and better functioning capital markets, making it easier for entrepreneurs to raise equity or debt. Debt, more common in the US than in Europe and certainly in Japan, acts as a potential growth multiplier. Finally, do not forget that a small annual difference due to the growth-on-growth effect causes a large growth gap in the long term.

Figure 2: US economic growth versus EU-15 and EU

Source: World Bank, via Fredrik Erixon, Oscar Guinea and Oscar du Roy, Director, Senior Economist and Research Assistant at ECIPE; EU-15 are the first fifteen EU-countries, before the expansion in 1995

3) Less dependence on foreign countries

The US has also become an autonomous region. Thanks to the rapidly scaled-up shale energy industry, they are also energy self-sufficient. Europe has become too dependent on Russia, among others, so that European consumers and companies now have a much higher energy bill than consumers and companies in the US and the rest of the world. Politically, too, Europe is still dependent on the US, whose military power sets the geopolitical agenda and can even ban ASML from exporting its machines to China.

4) 'Positive' influence private equity

In the US, the market for private equity and venture capital is better developed than in Europe. That keeps public companies sharp, in the sense that they have to ensure stable cash flows, otherwise private equity will start breathing down the neck of the directors. Companies also try to ward off private equity by purchasing shares. Private capital also facilitates the start-ups. A private equity fund like Sequoia Capital was at the cradle of Apple, Cisco, Google, Nvidia, Airbnb, Palo Alto Networks, ServiceNow, YouTube, Snowflake, Stripe and Whatsapp, among others.

5) Well-functioning currency union

Another striking difference between the US and the eurozone is the functioning of the monetary union. The US is a so-called ‘Optimal Currency Area’ (OCA). Broadly speaking, economic growth between the Member States is fairly equal, there is free movement of capital, goods and people, and transfers take place in the event of shocks. The euro is not an OCA. This even demonstrably hinders economic growth. The eurozone has a lower growth rate than European countries without the euro. We must either quickly complete the eurozone or move to another system.

6) Dominant reserve currency

Thanks to the well-functioning monetary union and the fact that the US is a (military) world power with a large share of the world market, the dollar is the world's reserve currency. Trading in commodities is largely settled in dollars. In South America, the dollar is de facto the currency of choice. Because dollars - even outside the US - are not always held in cash, the US government can easily finance itself with issues of T-bills.

Efforts are being made to break the power of the dollar, for example with the euro and the renminbi. But those coins are not yet perfect. The dollar is also a safe haven in times of stress, which gives US equities extra appeal from a diversification point of view.

7) The rise of passive investing

A less obvious explanation for the good performance of US equities is the rise of passive investing. Passive investing, market capitalization weighted indices, favors large companies. And the US dominates the world ranking of large companies. Nine of the ten largest companies are from the US (the only "dissonant" being Saudi Aramco).

As I have argued earlier, passive investing is engaging in politics. Passive investors 'subsidize' the big mega players from the US, at the expense of Europe.

Lagging behind the US is salient

The US is far from flawless. Much economic growth has taken place on credit. The mountain of debt is enormous, especially that of the US government. The inequality between the social upper and lower strata is very large. Recently, life expectancy in the US has also fallen. The country is also becoming an oligarchy, with too much influence from megacorporates. The fact that Europe is lagging far behind in this perspective can be called salient, all the more so as the EU needs the American big tech for various plans, such as the digital euro.

Finally, a new awakening?

A reviewer from Dagblad de Limburger described Grand Hotel Europa as 'a love letter to an old lover, a dead tired but beautiful continent'. At the end is one of the most bizarre endings of a literary book, one that should here symbolize the burial of old Europe (and possibly a new beginning).

With European cooperation, through the EU, we are trying to breathe new life into the continent. In fact, the EU is trying to make Europe a new power on the world stage. The question is whether the EU isn't too undemocratic and too power-hungry in this endeavor, and isn't suffocating the individual strengths and unique cultural differences between the countries too much. But that's a discussion for another time.

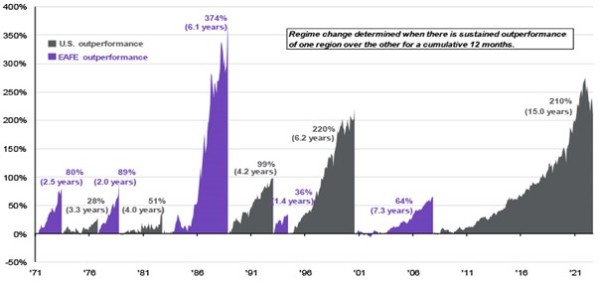

The US outperformance relative to the rest of the world (Europe/Africa/FarEast: EAFA) has reached a record not only in size, but also in duration (see Figure 3). It mainly went wrong for Europe after the credit crisis, also because long-term toxic American mortgage bonds were the most important export product to Europe. Figure 3 also shows that there are always cycles in relative performance. So Europe can also come back. The question is how and when.

Figure 3: Periods of relative outperformance US (grey) and EAFA (purple)

Source: FactSet, MSCI, J.P. Morgan AM (per 30/9/2022)

Even Ukraine's defeat of Russia will probably only be a temporary panacea. Or the US itself should implode. Then there is outperformance for lack of better. Incidentally, this is not a plea for the investment portfolio to consist only of US equities. After all, we always have to diversify and partly because of the low valuation, many European companies are quite interesting to include in the portfolio.

This article contains a personal opinion of Harry Geels