State Street SPDR ETF: Summer Winds Blowing In?

State Street SPDR ETF: Summer Winds Blowing In?

The first five months of 2022 have been punishing for bond market investors. There are some hints, though, that the winds are changing direction, for the US market at least. Despite recent volatility, the yield on the 10-year US Treasury is still more than 10bp off the recent highs, which has helped to stabilise other markets, notably investment grade credit. Its longer duration versus pure Treasury exposure and the spread widening seen on the back of concerns over the strength of the US economy have weighed on returns in 2022.

However, the paring back of interest rate expectations has facilitated the bounce in credit. Looking ahead, State Street SPDR ETFs sees four important areas for fixed income investors to consider when assessing investment grade credit.

Inflation concerns

CPI is high but at least it’s no longer rising, with the YoY rate dropping to 8.3% in April from 8.5%. The monthly May and June CPI readings were high in 2021, increasing the probability that the YoY rate will decline due to base effects. An ongoing pull-back in inflation may alleviate some of the pressure on the US Federal Reserve (Fed) to raise rates.

Peak rates

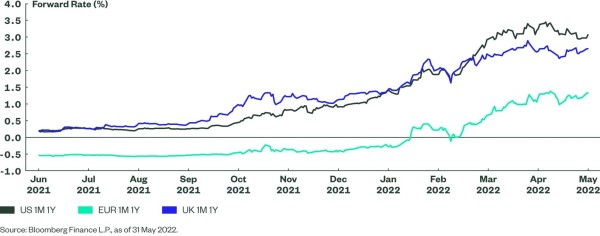

More limited expectations for policy tightening are already evident in the pricing of rate increases. The one-year forward of the US one-month rate – a decent proxy for where the market believes policy rates will be in a year’s time – has fallen back and is more than 15bp below the peak (see Figure 1).

This contrasts with the EUR forward rates, which have pushed to new highs above 1.5%. While longer-dated forwards do typically reach their highs closer to the end of the hiking cycle, the market has moved quickly to price in a rapid move in US policy rates to a more neutral level (3.0%). Unless it becomes clear that inflation is moving back higher or that growth is re-accelerating, there are limited reasons for expectations to shift above this level at this juncture.

Growth slowdown?

Fears that the Fed would over tighten and kill growth have pushed credit spreads to their widest in almost two years. However, growth has held up relatively well, with indicators such as the ISMs remaining comfortably above 50, suggesting economic expansion continues. There are few signs of financial distress yet as the upgrades to downgrades ratio for investment grade companies in North America sits comfortably above one in Q2 for both S&P and Moody’s ratings agencies.

Yield grab

The combination of the rise in US Treasury yields and spread widening has seen the yields on investment grade strategies push higher. The yield to worst on the Bloomberg US Corporate Bond Index reached close to 4.5%, which is near the highs seen in the COVID crisis and higher than the peak in 2018.

Figure 1: 1-Year Forward of the 1-Month Rate – US Rate Expectations Rolling Over

Jason Simpson, Senior Fixed Income Strategist at State Street SPDR ETFs:

"Flows into US investment grade corporate ETFs picked up into the end of May as investors potentially positioned for a rebound. The key risk is that inflation continues to surprise on the upside, but this appears more of an issue for Europe at the moment. As seen in Figure 1, it is much less clear that central bank rate expectations are rolling over in Europe, meaning we continue to favour short-duration strategies for European investment grade exposure.

For US credit, an all-maturity exposure now seems more appropriate. It has a longer duration than an all-Treasury index and, given the potential for spread compression following the widening seen year to date, makes investment grade credit look like one of the better ways to position for a bounce in the rates market. If gains prove short-lived and the market stabilises, then the higher yields on investment grade exposures should provide some additional returns. Spreads on the Bloomberg US Corporate Bond Index provide around a 130bp pick-up in yield to a similar duration Treasury index.

Lastly, the compression of US and European interest rate spreads has started to hurt the USD. For EUR-based investors concerned that this is a part of a bigger slide in the USD, currency hedging is always an option."

Share this post!

Related posts

-

Read more about "Fidelity: Strategische assetallocatie houdt recordinstroom ETF’s op gang"

Read more about "Fidelity: Strategische assetallocatie houdt recordinstroom ETF’s op gang"Fidelity: Strategische assetallocatie houdt recordinstroom ETF’s op gang

-

Read more about "DWS: ETF-markt blijft groeien in 2026"

Read more about "DWS: ETF-markt blijft groeien in 2026"DWS: ETF-markt blijft groeien in 2026

-

Read more about "Fidelity: Twijfel over AI drukt instroom Amerikaanse ETF’s"

Read more about "Fidelity: Twijfel over AI drukt instroom Amerikaanse ETF’s"Fidelity: Twijfel over AI drukt instroom Amerikaanse ETF’s

-

Read more about "Invesco: Instroom ESG-ETF’s hoogste sinds 2023"

Invesco: Instroom ESG-ETF’s hoogste sinds 2023

-

Read more about "BlackRock: Veel Nederlandse jongeren stappen in ETF’s uit fomo-overwegingen"

BlackRock: Veel Nederlandse jongeren stappen in ETF’s uit fomo-overwegingen

-

Read more about "Vanguard: Recordinstroom nu de vraag naar obligatie-ETF's sterk stijgt"

Vanguard: Recordinstroom nu de vraag naar obligatie-ETF's sterk stijgt

-

Read more about "Schroders: Waarom active ETF’s zo goed werken"

Schroders: Waarom active ETF’s zo goed werken

-

Read more about "Wim Zwanenburg: ETF boom or ETF bubble?"

Read more about "Wim Zwanenburg: ETF boom or ETF bubble?"Wim Zwanenburg: ETF boom or ETF bubble?

-

Read more about "Fidelity: Recordinstroom in obligatie-ETF's"

Fidelity: Recordinstroom in obligatie-ETF's

-

Read more about "Fidelity: Instroom in ETF’s bereikt hoogste niveau ooit in september"

Fidelity: Instroom in ETF’s bereikt hoogste niveau ooit in september