Fidelity: Rising rates aren’t always bad for ‘low vol’ strategies

Fidelity: Rising rates aren’t always bad for ‘low vol’ strategies

Rules of thumb are attractive, but that doesn’t mean they always work. For example, rising bond yields don’t automatically mean bad news for low volatility strategies; understanding why requires a closer look at the driving forces to each cycle of rate increases.

One common presumption about low volatility investment strategies is that they will underperform during periods of rising interest rates. This is because they are often biased towards rate-sensitive defensive sectors like healthcare, telecommunications, consumer staples, and, more recently, tech.

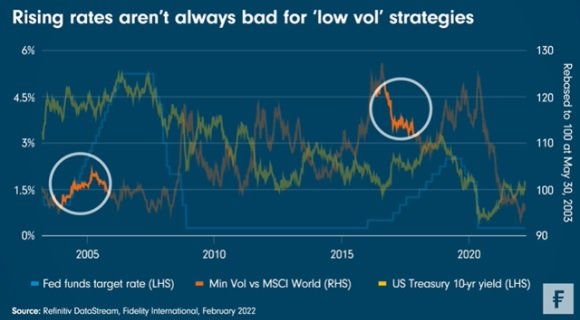

But that is not always the case. As the US Federal Reserve eyes a new cycle of interest rate increases, it’s worth taking a look at what happened the last time around. Indeed, the historical performance of the MSCI World Minimum Volatility Index versus the MSCI World Index during the last two US rate hiking cycles reveals a more nuanced picture. Contrary to conventional wisdom, the ‘Min Vol’ index actually outperformed through the early and mid-stages of the 2004-2005 hiking cycle, before drifting lower towards the end. In contrast, the ‘Min Vol’ index underperformed for most of the 2016-2018 hiking cycle.

Goldilocks scenario

The difference? The 2004-2005 cycle was a steady tightening of policy, which helped anchor long-term Treasury yields and the US Dollar index. This was a Goldilocks scenario for global equities, including low volatility stocks. By contrast, in 2016-2018, Treasury yields roughly doubled while real yields remained stable, reflecting a rise in inflation that outpaced real growth. The resulting ‘hunt for growth’ led defensive sectors to underperform.

So what should investors expect from the coming cycle of rate hikes? An extensive monetary tightening profile is already priced into markets. But there are good reasons to think there is a limit to how far and how fast interest rates and long-term bond yields can rise, given the ‘Catch-22’ dilemma facing central banks. As Fidelity CIO Andrew McCaffrey explains, GDP growth appears to have already peaked and economies remain acutely sensitive to higher financing costs due to a huge debt burden. Therefore, while inflation remains an issue, it is likely that the tightening cycle won’t be as steep as markets expect.

Even if rates do rise quickly, different types of ‘low vol’ strategies will respond in different ways. This will depend crucially on how a low volatility portfolio is built and managed. For example, integrating forward-looking research inputs could help to pre-emptively avoid stocks with increasing rate risk, while the sector composition of dynamically run strategies will shift over time as parts of the market with increasing volatility are reduced. Investors can also take a regional approach to low volatility equities, with a focus on parts of the world - like Europe - where there is less upside risk to bond yields for particular ‘low vol’ sectors.

Share this post!

Related posts

-

Read more about "Nuveen: Amerikaanse obligatiemarkt oogt rustig, terwijl rente oploopt"

Read more about "Nuveen: Amerikaanse obligatiemarkt oogt rustig, terwijl rente oploopt"Nuveen: Amerikaanse obligatiemarkt oogt rustig, terwijl rente oploopt

-

Read more about "RBC BlueBay AM: Escalatie Groenland kan rentes wereldwijd hoger zetten"

Read more about "RBC BlueBay AM: Escalatie Groenland kan rentes wereldwijd hoger zetten"RBC BlueBay AM: Escalatie Groenland kan rentes wereldwijd hoger zetten

-

Read more about "RBC BlueBay: Rentecurve steiler door obligatieverkopen pensioenfondsen"

Read more about "RBC BlueBay: Rentecurve steiler door obligatieverkopen pensioenfondsen"RBC BlueBay: Rentecurve steiler door obligatieverkopen pensioenfondsen

-

Read more about "LFDE: In de renteklem"

Read more about "LFDE: In de renteklem"LFDE: In de renteklem

-

Read more about "Nuveen: Renteverlagingen Fed raken verder uit zicht door hardnekkige inflatie"

Read more about "Nuveen: Renteverlagingen Fed raken verder uit zicht door hardnekkige inflatie"Nuveen: Renteverlagingen Fed raken verder uit zicht door hardnekkige inflatie

-

Read more about "Han Dieperink: The law that investors keep forgetting"

Read more about "Han Dieperink: The law that investors keep forgetting"Han Dieperink: The law that investors keep forgetting

-

Read more about "PGIM: Grote verschillen onder de oppervlakte binnen bedrijfsobligaties"

Read more about "PGIM: Grote verschillen onder de oppervlakte binnen bedrijfsobligaties"PGIM: Grote verschillen onder de oppervlakte binnen bedrijfsobligaties

-

Read more about "Vanguard: AI en rente bepalen de risico's en kansen dit jaar"

Read more about "Vanguard: AI en rente bepalen de risico's en kansen dit jaar"Vanguard: AI en rente bepalen de risico's en kansen dit jaar

-

Read more about "DNB: Multinationals verstrekken ruim € 150 mld aan leningen aan Nederlandse bedrijven"

Read more about "DNB: Multinationals verstrekken ruim € 150 mld aan leningen aan Nederlandse bedrijven"DNB: Multinationals verstrekken ruim € 150 mld aan leningen aan Nederlandse bedrijven

-

Read more about "BlackRock: Obligaties weer aantrekkelijk, Europa in de spotlight"

Read more about "BlackRock: Obligaties weer aantrekkelijk, Europa in de spotlight"BlackRock: Obligaties weer aantrekkelijk, Europa in de spotlight