Capital Group: Kansen in volatiele tijden

Capital Group: Kansen in volatiele tijden

")

De vrees voor een aanhoudende inflatie en een verstrakking van het monetaire beleid heeft de markten sinds het begin van het jaar opgeschrikt. Relatief hoog geprijsde sectoren zoals de technologiesector hadden aanvankelijk het zwaarst te lijden onder de sell-off omdat hun waarderingen kritisch onder de loep werden genomen vanwege de verwachting dat de rente kan gaan stijgen.

De volatiliteit breidde zich uit naar blue chip-aandelen, waarbij de S&P's 500 Composite Index op maandag kortstondig in correctiegebied kwam, alvorens weer op te krabbelen. Op woensdag sputterden de markten opnieuw, toen de Federal Reserve liet doorschemeren dat ze mogelijk sneller dan verwacht de rente gaat verhogen en haar balans gaat inkrimpen.

Ook nieuwe geopolitieke spanningen, variërend van de grenscrisis tussen Rusland en Oekraïne tot de betrekkingen tussen de VS en China, wakkeren de onzekerheid op de markten aan en zullen de activaprijzen de komende maanden waarschijnlijk onder druk houden. Toch denken enkele specialisten van Capital Group dat de markten gezonder zijn dan veel beleggers menen.

Hieronder volgen hun ideeën over hoe de marktcorrectie en het nieuwe beleid van de Fed een kans bieden om portefeuilles aan te passen, met het oog op de komende drie tot vijf jaar.

Growth sectors still present opportunities

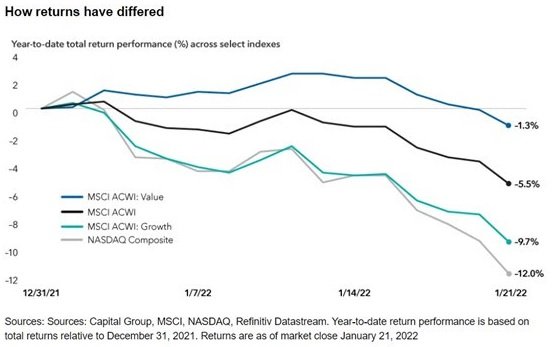

The severity of the market correction reflects an increasingly risk-off investor sentiment, hitting expensively valued growth stocks and speculative assets like cryptocurrencies particularly hard. Meanwhile, more value-oriented stocks in areas of energy, financials and consumer staples have fared better, suggesting that a longer term market rotation may be taking root.

The NASDAQ Composite fell 7.6% last week, suffering its biggest decline since the start of the pandemic. As of January 26, 44% of stocks in the NASDAQ Composite were down 50% or more from their 52-week highs.

Netflix was among the hardest hit last week when its share price fell 22% on January 21 after reporting lower-than-expected subscriber growth. This triggered deeper concerns that even industry giants would not be spared from eroding demand, tougher competition and potentially deteriorating earnings. Within the technology sector, recent price action indicates investor preference for high-quality, low price-to-earnings (P/E) companies over the higher valued companies which tend to be more sensitive to rising rates.

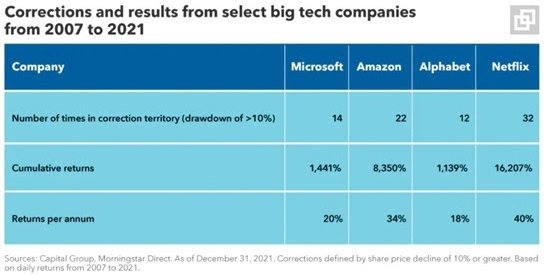

But volatility in the share prices of emergent companies is to be expected. Over the past 15 years, some fast-growing companies have experienced multiple corrections in share price. Those investors who weathered the market turbulence and remained invested would have realized attractive returns however.

In short, earnings matter. History has shown that certain high multiple companies can continue to appreciate should fundamentals exceed expectations over time. This is especially true for select growth companies with large and expanding total addressable markets with potentially long revenue and earnings growth runways.

This week’s news from the Fed was a bit more hawkish than the market anticipated but it doesn’t change our outlook for the year. We continue to expect at least four (25 basis point) rate hikes and think inflation is likely to persist well above the Fed’s target this year. We have been thinking that a faster pace of rate hikes can’t be ruled out, and Powell’s comments at the press conference confirmed this.

The last time the Fed hiked, it did so in 25 basis point increments each quarter. That is still probably its most likely course of action this time, but given how far above target inflation is, there's no reason why the Fed would want to limit its ability to hike faster if it needs to. In his comments to the press, Powell did not dismiss the possibility that the Fed would speed up tightening or rule out the possibility of raising rates in 50 basis point increments.

Investors could be in for a turbulent ride over the next few quarters. It may not take many rate hikes or much quantitative tightening to spur more equity market volatility. But the view of Capital Group’s rates team is that the Federal Reserve is not likely to let the stock market throw it off the path of tightening, like it did in the last hiking cycle. If you go back to 2017 and 2018, when the Fed hiked 175 basis points, it had space to reverse course when asset prices plunged because inflation was below target. Today that is not the case.

This would present a tricky dilemma for the central bank. It would be hard for the Fed to claim to be credible about achieving its dual mandate (of promoting price stability and full employment) if it backs off of its tightening schedule before inflation comes down.

Although any period of monetary tightening can generate higher market volatility, U.S. equities could remain supported by earnings growth. And while valuations are high relative to history, they are not exorbitant considering current and projected levels of interest rates.

I believe that S&P 500 earnings can grow 8% to 10% in 2022, which is still a respectable rate considering the strong rebound in corporate earnings last year. In addition, while inflation is certainly a concern for overall economic conditions, it can be beneficial for earnings growth.

Recent data would seem to indicate that inflation may persist for longer than expected and the Fed could be forced into a more aggressive tightening cycle than previously anticipated. While history suggests that tighter monetary policy and higher rates almost always put downward pressure on equity valuations, what this means for market levels depends on earnings growth and how much it can offset a contraction in price-to-earnings (P/E) multiples.

In fact, perhaps contrary to conventional wisdom, the market has tended to rise in periods following initial increases in the federal funds rate. The exceptions to this are the inflationary periods of the 1970s and early 1980s, in addition to periods when the S&P 500 P/E ratio was more than 20 times earnings at the time of the initial tightening — periods which, of course, have some similarity to today.

However, inflation then was significantly worse and accompanied by a deep recession. In addition, interest rates in prior periods of high valuation were substantially higher. While this is no guarantee that the equity market won’t decline when the Fed tightens, it does provide a bit more support than was evident during some of those historical episodes.

My base case scenario is for U.S. GDP to grow 2% to 3% in 2022 as fiscal stimulus wanes and monetary policy tightens. This slower — but still positive — economic growth should support an increase in corporate profits.

While we are not likely to see the outsized gains of 2021, single-digit equity returns still seem attainable as the market rises in line with, or slightly less than, earnings growth this year. They are likely to be accompanied by more volatility, and we are starting to see that in markets. And while a correction is never out of the realm of possibility in any given year or economic environment, we do not expect a systemic market decline given current economic conditions, earnings strength and level of interest rates.

Share this post!

Related posts

-

Read more about "Harry Geels: Global Titans conquer the world"

Read more about "Harry Geels: Global Titans conquer the world"Harry Geels: Global Titans conquer the world

-

Read more about "Han Dieperink: Europapa"

Read more about "Han Dieperink: Europapa"Han Dieperink: Europapa

-

Read more about "Bob Homan: We are starting to look like hedge fund managers"

Read more about "Bob Homan: We are starting to look like hedge fund managers"Bob Homan: We are starting to look like hedge fund managers

-

Read more about "Han Dieperink: The negative small cap premium"

Han Dieperink: The negative small cap premium

-

Read more about "Han Dieperink: The Magnificent Seven, great promise or bubble?"

Read more about "Han Dieperink: The Magnificent Seven, great promise or bubble?"Han Dieperink: The Magnificent Seven, great promise or bubble?

-

Read more about "Bob Homan: Right for the wrong reasons"

Bob Homan: Right for the wrong reasons

-

Read more about "Bob Homan: Very surprising, how investors can be surprised"

Bob Homan: Very surprising, how investors can be surprised

-

Read more about "Bob Homan: Very surprising, how investors can be surprised"

Bob Homan: Very surprising, how investors can be surprised

-

Read more about "Han Dieperink: European equities are justifiably cheap"

Han Dieperink: European equities are justifiably cheap

-

Read more about "Bob Homan: How seven Wild West heroes put the stock market to their liking"

Bob Homan: How seven Wild West heroes put the stock market to their liking