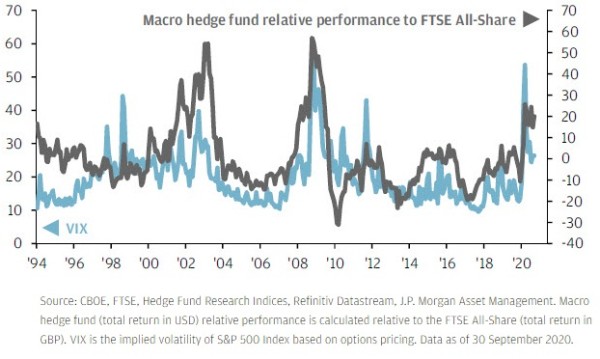

JP Morgan: Macro hedge funds have tended to outperform equities when volatility rises

JP Morgan: Macro hedge funds have tended to outperform equities when volatility rises

In the final quarter of this year, investors are likely to learn the answers to three pivotal questions for markets.

First, we are likely to hear the results of vaccine trials. Second, we will learn the results of the US election, which could have important policy implications, including the potential for further fiscal stimulus. Finally, we will see whether a deal can be reached between the UK and European Union. If the answer to any of these questions generates significant volatility, macro hedge funds have historically been a good source of diversification in portfolios. Meanwhile, if we get positive answers to all three questions, the most flexible macro strategies that can rapidly increase their equity exposure could then capture some of the likely resulting upside to equity markets while having buffered portfolios during this year’s volatility.

Index level (LHS); % change year on year (RHS)

Share this post!

Related posts

-

Read more about "Brava Finance: Asset managers predict boom in digital asset allocations"

Read more about "Brava Finance: Asset managers predict boom in digital asset allocations"Brava Finance: Asset managers predict boom in digital asset allocations

-

Read more about "DNB: Risico’s door exposure naar techaandelen nemen toe"

Read more about "DNB: Risico’s door exposure naar techaandelen nemen toe"DNB: Risico’s door exposure naar techaandelen nemen toe

-

Read more about "BlackRock: Barsten in het concept van portefeuillediversificatie"

Read more about "BlackRock: Barsten in het concept van portefeuillediversificatie"BlackRock: Barsten in het concept van portefeuillediversificatie

-

Read more about "RBC Global AM: Aandelen uit opkomende markten op een keerpunt"

Read more about "RBC Global AM: Aandelen uit opkomende markten op een keerpunt"RBC Global AM: Aandelen uit opkomende markten op een keerpunt

-

Read more about "Brava Finance: Digital assets are a strategic priority for wealth managers"

Brava Finance: Digital assets are a strategic priority for wealth managers

-

Read more about "Schroders: Amerikaanse aandelenmarkten blijven de toon zetten"

Read more about "Schroders: Amerikaanse aandelenmarkten blijven de toon zetten"Schroders: Amerikaanse aandelenmarkten blijven de toon zetten

-

Read more about "Han Dieperink: Party like it's 1999"

Read more about "Han Dieperink: Party like it's 1999"Han Dieperink: Party like it's 1999

-

Read more about "LFDE: Wie waagt de (cyber)sprong?"

Read more about "LFDE: Wie waagt de (cyber)sprong?"LFDE: Wie waagt de (cyber)sprong?

-

Read more about "Allspring Global Investments: Shifting tides - EM equities back in focus"

Read more about "Allspring Global Investments: Shifting tides - EM equities back in focus"Allspring Global Investments: Shifting tides - EM equities back in focus

-

Read more about "AllianzGI: Tien redenen om Chinese aandelen (opnieuw) te overwegen"

Read more about "AllianzGI: Tien redenen om Chinese aandelen (opnieuw) te overwegen"AllianzGI: Tien redenen om Chinese aandelen (opnieuw) te overwegen