State Street SPDR ETFs: Anticipating the top to the monetary policy cycle

Expectations suggest that the end of the Fed’s rate hiking cycle could be nearing. US investment grade credit has seen a material re-pricing and, looking at the previous hiking cycle (2016-2018), this exposure started to gain traction once markets believed the final rate hike had taken place. Is it now time to revisit investment grade credit?

Central banks continue to focus on inflation, with the ECB, Fed and BoE all opting to hike rates. As such, they have tried to put some space between the objectives of monetary policy (controlling inflation) and the task of managing issues in the banking system.

However, tighter credit conditions as a result of the challenges in the banking sector do change the dynamic for the economy. So while the immediate crisis may have abated, central banks largely concede that tighter credit conditions point to the top to the monetary policy cycle being close at hand.

The issues in the banking sector have not been easy for asset markets to navigate. There are now real fears that the policy tightening that has already been delivered, coupled with tighter credit conditions, could tip growth into negative territory. On the back of this worry, there has been a risk-off switch to more defensive strategies, such as money market funds, but the point of maximum pressure seems to have passed with markets now more stable.

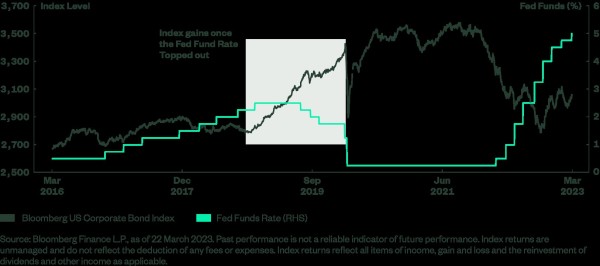

An opportunity in US Investment Grade Credit

Jason Simpson, Senior Fixed Income Strategist at State Street SPDR ETFs:

'Although risks remain, US investment grade bonds have undergone a material re-pricing. Spreads to Treasuries blew out to the wides seen in October 2022, the point of peak bearishness in markets. Spreads have reversed some of that move but remain at 145bp for the Bloomberg US Corporate Index, well above the 115bp it hit in early February and 20bp wide to the 10-year average. This gives the index a yield to worst of close to 5.2%. Credit spreads therefore offer some protection against a US economic slowdown. This spread to the underlying ‘risk-free rate’ is one component of returns, the other being what happens to underlying Treasury yields. This is typically dependent on the stage of the monetary policy cycle and, as already indicated, expectations are that the end of the Fed rate cycle is close.

While each cycle is different, Figure 1 shows the 2016-2018 Fed tightening cycle and how, during that cycle, returns from the Bloomberg US Corporate Index were fairly flat until late 2018. Positive returns from the index started to feed through in a more sustained manner once the market seemed sure that the final hike was in place. Gains stretched through into 2020, only undergoing a serious correction as markets priced in the big hit to GDP from COVID. A large part of those returns came from the rally in the underlying Treasury curve.'

Figure 1: US Corporate Returns Gained Traction as the Last Fed Hike of the 2016-2018 Cycle Came