Harry Geels: Government and business are becoming more entangled

")

This column was originally written in Dutch. This is an English translation.

By Harry Geels

The era of completely free markets is long gone. Over the last two decades, Western governments have built up increasingly significant stakes in companies. This has important implications for investors.

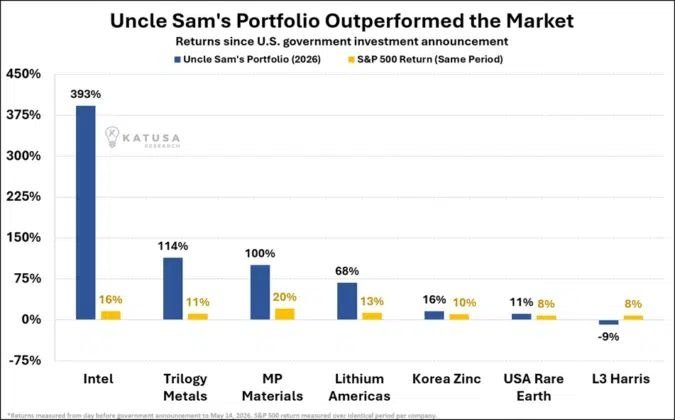

The trade war that the US is waging against various ‘partners’ around the world is not just about trade tariffs. Since 2025, the US government has also been investing in all manner of ‘strategic’ companies, through shareholdings, subsidies (grants, the IRA, the CHIPS Act), loans or guarantees, defence contracts and strategic partnerships. The chart below shows seven companies in which the US government has built up a significant stake, also known as ‘Uncle Sam’s Portfolio’.

Source: Katusa/via Charles-Henry Monchau

Such partnerships are not unique to the US. Europe is no stranger to them either. Such stakes are often justified on the grounds of strategic or geopolitical necessity. China, of course, is also notorious for its so-called SOEs (State-Owned Enterprises), which are partly owned by the government and partly by the public. Let us first discuss some notable examples of government intervention, before examining what this means for the system and for investors.

Examples

The government’s renewed role is most clearly evident in what policymakers themselves refer to as ‘strategic sectors’. In the US, tens of billions in subsidies are flowing into the semiconductor sector, with Intel serving as a well-known example of a company that is being put back on the map partly thanks to the CHIPS Act. The same pattern is repeated in critical raw materials: lithium producers and rare-earth companies such as MP Materials are benefiting from cheap loans, guarantees and long-term supply security.

The same applies to the space and defence sectors, where companies such as SpaceX effectively operate on a continuum between private enterprise and public infrastructure, fuelled by substantial contracts with NASA and the Pentagon. Europe is following a similar path, albeit in more technocratic terms. Through programmes centred on ‘strategic autonomy’, companies such as ASML (EU Chips Act), Airbus and the local aviation sector are explicitly supported to safeguard global competitiveness.

At the same time, governments hold shares in banks, energy companies and telecoms infrastructure, or intervene when markets come under pressure, as was recently the case with the nationalisation of energy giants such as the German firm Uniper. This creates a hybrid system in which key sectors become structurally intertwined with public interests and capital, and in which policy is often coordinated – particularly in times of crisis – leading to conflicts of interest.

Corporate socialism

Due to the close intertwining of large companies and the state, capitalism in the classical sense no longer exists. Ideal-typical capitalism is characterised by mutual competition (for the benefit of customers), limited government, ‘price discovery’, and rewards and penalties via free markets.

In current practice, however, the government selects strategic sectors, capital flows follow policy, powerful oligopolies and monopolies emerge, and companies that are ‘too big to fail’ are bailed out.

This leads to enormous ‘wealth transfers’, for example from taxpayers, consumers, savers and small businesses to shareholders and employees of large companies, debtors and the government. We would be better off calling the current system corporate socialism, crony capitalism, oligarchic capitalism or state capitalism. The term corporate socialism refers to a system in which profits are privatised and losses are socialised, in other words, passed on to the taxpayer.

Consequences for investors

Investors are ideologically in favour of the free market, but financially dependent on precisely the opposite. They welcome the extra profits generated by oligopolies and monopolies. We might call this the ‘investor’s paradox of market power’. Warren Buffett has amassed his wealth primarily by investing in such oligopolistic and monopolistic companies at opportune moments, although – to describe his strategy – he opts for more elegant phrasing, such as investing in companies with ‘pricing power’ or in sectors with high barriers to entry.

There is another lesson for investors. The graph above suggests that when the US government invests, this can lead to exceptional stock market returns. But a sample size of n=7 is, of course, not conclusive evidence. Research shows that such government interventions lead to greater market share and cheaper financing, but also to greater inefficiency. On balance, the outlook is slightly positive for investors, particularly in the shorter term, immediately following the announcement of the collaboration.

Finally, two further issues

How can we improve the system or make it fairer? If we accept that the government plays a strategic role in the economy and that oligopolies and monopolies are sometimes unavoidable, it stands to reason to examine how the benefits of these can be shared more widely. Consider employee share schemes, user or consumer participation, or skimming off monopoly profits and returning them to society, for example through lower taxes.

Perhaps an even more fundamental question is: who actually controls whom? In a system where government and the business sector become so closely intertwined, not only does the boundary between market and state become blurred, but so does the line marking where power ultimately lies. One political camp points to the powerful government, the other to the powerful business sector, resulting in confusion and polarisation.

One way out of this is to recognise the shades of grey in the current system. Only when we analyse more closely how our economy actually works and how the system can best be described (see suggestions above) can we also have a more meaningful discussion about how it ought to work.

This article contains a more personal opinion by Harry Geels