Harry Geels: Greece, from debt crisis to market darling

This column was originally written in Dutch. This is an English translation.

By Harry Geels

The country that, a decade ago, was synonymous with mismanagement, debt restructuring and political chaos is once again being embraced by investors. There are broadly four reasons to take a more positive view of Greece. Taken together, they provide an excellent case study for both economists and investors.

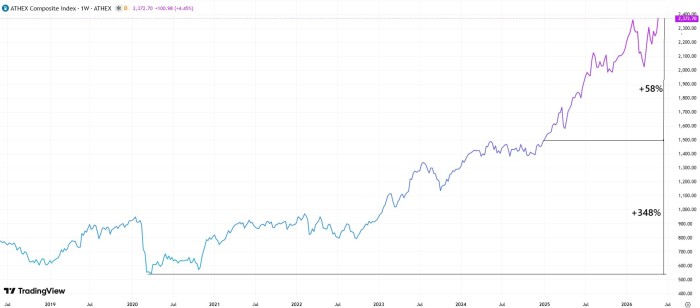

In recent years, the Greek stock market has been among the best-performing European stock markets. Since the start of 2025, the ATHEX Index has risen by around 58%. Since the low point of the coronavirus crisis, it has risen by as much as 348%. By way of comparison, since the coronavirus slump, the AEX investment index has ‘merely’ doubled. The ATHEX Index comprises around sixty shares, but is highly concentrated: a small group of top performers dominates the index, with the ten largest shares accounting for roughly three-quarters of the total, including several banks.

It is not always easy to pinpoint a single clear cause for the current performance. Several factors are at play, reinforcing one another. Thanks to roughly four developments, Greece is in a better position than it was fifteen to seventeen years ago, when the country was ravaged by a euro and debt crisis and the so-called Troika – consisting of the IMF, the European Commission and the ECB – had to intervene through emergency loans and imposed austerity measures and restructuring.

The legacy of the Troika

The austerity measures and reforms imposed by the Troika were socially and politically costly, but have helped lay the foundations for the current recovery. Public finances have been drastically cleaned up and structural deficits have been turned into surpluses. The economy has become more flexible and competitive as a result of adjustments to the minimum wage, the retirement age and tax structures. Under strict conditions, access to external financing was restored and improved.

At the time, there was much criticism of the ‘tough measures’. Terms such as ‘austerity experiment’, ‘punitive austerity’ and even ‘economic occupation’ were used. It was also argued that the bailout of Greece was in fact also a bailout of Northern European banks, which had invested heavily in Greek government bonds. Finally, serious questions were raised about the democratic legitimacy of the measures. The Greek parliament effectively had only two choices: to agree or to let the country go bankrupt.

Incidentally, there is a broader lesson here. At the time, Greece had a large amount of outstanding debt to external investors, particularly Western banks (which were allowed to hold Greek government bonds as capital without a discount) and hedge funds (which profited from relatively higher interest rates on seemingly safe loans). A country that borrows externally has to deal with external parties during a restructuring, who ultimately help to set the agenda. In such a situation, sovereignty is severely curtailed in practice, something we also regularly see in emerging markets.

Bank balance sheet recovery

The second part of the story is the recovery of the financial sector. The balance sheets of Greek banks, which were partly responsible for the crisis of confidence, have been cleaned up. The number of non-performing loans has been drastically reduced and lending has picked up again. As a result, investment is picking up, consumption is picking up and property markets are recovering. The construction sector in particular is benefiting visibly, not only from domestic demand but also from foreign (tax-related) inflows.

Capital and people are returning

Thirdly, what is often overlooked is that Greece is gradually assuming a new position within Europe. The country is no longer just a tourist destination, but also a place to live and invest. Three factors are coming together: tax attractiveness (relatively favourable regimes for wealthy newcomers), quality of life (climate, cost of living, and Athens, which is starting to buzz again) and relatively low-priced property. As a result, part of the Greek diaspora is returning.

Europe is chipping in

Furthermore, Europe is playing a crucial role. Greece is one of the largest recipients of the European Recovery Fund. The billions invested in infrastructure, digitalisation and the energy transition are supporting growth. But perhaps even more important is the institutional anchoring. With implicit support mechanisms within the eurozone, including the ECB’s safety net, the stability of the system has increased. The risk of a ‘Grexit’, once a daily topic of conversation, has completely disappeared. This brings down the risk premium, and it is precisely this that translates into higher stock market valuations.

Why the stock market is performing so strongly

The strong performance of the Greek stock market is not only a result of improved fundamentals, but also of various ‘market technicalities’. The market is small and concentrated, banks play a dominant role, and it is precisely this sector that has recovered strongly. During the crisis, international investors pulled out of Greece. Now that they are returning, we are seeing a typical ‘outsized effect’: relatively limited capital flows are having a disproportionately large impact on share prices. The upgrade to investment grade and the renewed inclusion in allocation models mean that capital flows are relatively large compared to the size of the market.

The downside

And therein lies the risk. For although Greece’s story has become more convincing, it is still not a risk-free investment. The economy remains relatively small and vulnerable to external shocks. Tourism still plays a dominant role. The debt ratio remains high, despite improvements. And the stock market is concentrated and illiquid. For investors, this means that the recent outperformance is not automatically an invitation to concentrate holdings.

In conclusion

Greece is no longer a problem case, but neither is it a cornerstone of the portfolio, insofar as it ever was. It is an interesting and instructive recovery story that has now evolved into a revaluation story. Reforms and far-reaching adjustments have clearly contributed to this recovery. Perhaps a lesson for France, which in terms of its debt-to-GDP ratio is approaching a level comparable to that of Greece in the early phase of the crisis (>120%), albeit in a completely different institutional context. The Greek stock market is not rising because everything is perfect, but because the direction is finally right.

This article contains the personal opinion of Harry Geels