Seb Beloe: Impact investing challenges in listed equities

Seb Beloe: Impact investing challenges in listed equities

The popularity of ESG and sustainable investing has increased dramatically over the past few years. Impact investing is no exception to this trend. However, the rapid growth in impact investing has led to concerns about weakening standards in listed equities.

By Seb Beloe, Partner and Head of Research, WHEB Asset Management

As impact investing has grown, it has attracted new participants. This has led to concerns over a weakening of standards. The 2020 Annual Impact Investor Survey1 identified ‘impact washing’ as the greatest challenge facing the market. Transparency and authenticity have become essential but differentiation between funds is becoming increasingly challenging.

Understanding what ‘impact investing’ means is the first step in clarifying the parameters used to assess asset managers in this space. Asset managers need to decide whether they want to take a holistic or a traditionalist approach to impact investing, whether intentionality or additionality is the core objective.

A traditionalistic view versus a holistic view

We distinguish between traditionalistic and holistic views of impact investing. The traditionalistic view holds that an investor’s impact needs to be ‘additional’. That is, any positive outcome would not have occurred but for that investor’s specific investment.

Within this view, it is not sufficient to measure and report positive changes in outcomes – usually emanating from a change in the cost of capital – and point to a causal link between the investment and these outcomes. It also requires that the investor is the only available capital provider for an asset, and that the positive impact would not materialise without the investment.

Other types of investor impact, such as engagement with investee companies, furthermore do not qualify under this interpretation. This is because documenting a causal link that asserts additionality is so difficult. It is rarely possible to attribute a specific outcome to a particular engagement activity.

A holistic approach focuses instead on investments as part of the financial system. This view holds that investor impact is founded in the investor’s intention to deliver positive impact and is then delivered through investor contributions. These contributions can include changes in the cost of capital and engagement with the underlying enterprise as well as wider signalling to other market participants. This holistic view acknowledges the ‘intense’ impact generated by investors demonstrating additionality, but also embraces a spectrum of more ‘diffuse’ positive impact delivered through other mechanisms.

Listed equity impact investing isn’t different

A common extension of the traditionalistic view is that ‘real’ impact investing cannot happen in listed equities because shares in listed companies are just traded between investors. The big error to avoid here is to see the listing of shares as a differentiator. When shares trade on a listed market, ownership changes without direct capital introduction. But the same can be the case for transactions in private markets.

Intention over additionality

The difficulties in demonstrating additionality lead us to conclude that it does not offer a pragmatic test to determine whether an investor is an impact investor. Instead of focusing on whether an investment is additional or not, a more appropriate standard, aligned with the GIIN and IFC definitions, focuses on the investor’s intent.

In our view, this intention is at the core of what it means to be an impact investor. The impact needs to be a significant part of asset selection. Further, the investor needs to intend for the investment to contribute to positive impact and must be able to demonstrate how this impact is delivered.

This definition is also aligned with our clients, who see their capital as an extension of themselves and a way to project their values onto the world. Our role is to channel this capital to fulfil its purpose by intentionally directing it into companies that deliver positive impact.

Our holistic impact approach

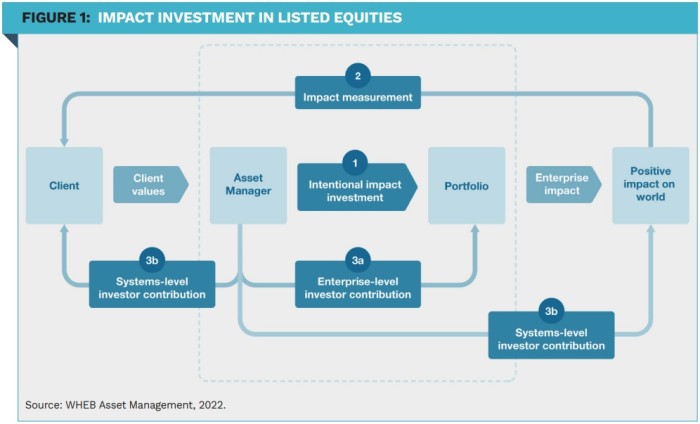

We are firmly in the ‘holistic impact’ camp. Our investment decision is explicitly rooted in the enterprise impact of the business (‘1’ in Figure 1). Our intention as an investor is to deliver positive impact at the level of the individual enterprise (‘3a’) and across the financial system (3b). We document and report on our investment intentions and contributions to underpin our claims to positive impact (2).

Establishing demanding but pragmatic standards that require clarity in investment intentions, and evidence of investor contributions, is essential if impact investment is to retain its potency. These standards will enable impact investors to harness the full potential of capital markets to drive positive impact at scale.

Impact investing and cost of capital

The traditionalistic view holds that impact investing in listed equities is not possible. Apparently, listed equity investors are unable to influence the cost of capital of investee companies.

However, we would argue that this perspective ignores the systemic nature of finance and the economic system.

|

SUMMARY There are two levels of impact in the investment valuechain. ‘Enterprise Impact’ is delivered by the underlying asset. Separately, ‘investor impact’ can be delivered by the investor themselves. A traditionalistic view of the investor impact focuses on additionality. This view is typically restricted to philanthropy or to markets with very poor liquidity. A ‘holistic’ approach focuses instead on the investor’s intention and is delivered through changes in the cost of capital, engagement and wider signaling. |

Attachments

Share this post!

Related posts

-

Read more about "PGGM neemt belang van 49% in Carbon Collectors"

Read more about "PGGM neemt belang van 49% in Carbon Collectors"PGGM neemt belang van 49% in Carbon Collectors

-

Read more about "RBC Global AM: Aandelen uit opkomende markten op een keerpunt"

Read more about "RBC Global AM: Aandelen uit opkomende markten op een keerpunt"RBC Global AM: Aandelen uit opkomende markten op een keerpunt

-

Read more about "Brava Finance: Digital assets are a strategic priority for wealth managers"

Read more about "Brava Finance: Digital assets are a strategic priority for wealth managers"Brava Finance: Digital assets are a strategic priority for wealth managers

-

Read more about "Schroders: Amerikaanse aandelenmarkten blijven de toon zetten"

Read more about "Schroders: Amerikaanse aandelenmarkten blijven de toon zetten"Schroders: Amerikaanse aandelenmarkten blijven de toon zetten

-

Read more about "Han Dieperink: Party like it's 1999"

Read more about "Han Dieperink: Party like it's 1999"Han Dieperink: Party like it's 1999

-

Read more about "LFDE: Wie waagt de (cyber)sprong?"

Read more about "LFDE: Wie waagt de (cyber)sprong?"LFDE: Wie waagt de (cyber)sprong?

-

Read more about "Allspring Global Investments: Shifting tides - EM equities back in focus"

Read more about "Allspring Global Investments: Shifting tides - EM equities back in focus"Allspring Global Investments: Shifting tides - EM equities back in focus

-

Read more about "Returns and impact of sustainability-labeled bonds (Roundtable 'Green, Blue & Orange Bonds' – part 2)"

Read more about "Returns and impact of sustainability-labeled bonds (Roundtable 'Green, Blue & Orange Bonds' – part 2)"Returns and impact of sustainability-labeled bonds (Roundtable 'Green, Blue & Orange Bonds' – part 2)

-

Read more about "AllianzGI: Tien redenen om Chinese aandelen (opnieuw) te overwegen"

Read more about "AllianzGI: Tien redenen om Chinese aandelen (opnieuw) te overwegen"AllianzGI: Tien redenen om Chinese aandelen (opnieuw) te overwegen

-

Read more about "Bob Homan: Give volatility time to run its course"

Read more about "Bob Homan: Give volatility time to run its course"Bob Homan: Give volatility time to run its course