Fidelity: Ukraine war cuts rate hike expectations

Fidelity: Ukraine war cuts rate hike expectations

The main global economic fallout of war in Ukraine is likely to be a stagflationary shock, as a result of severe disruption to commodity markets. The European Central Bank has already signalled a more cautious policy approach in response, as the risk of recession is rising. We expect the Federal Reserve to stick to its hawkish narrative for now but ultimately carry out fewer hikes than the market anticipates.

Russia’s invasion of Ukraine is first and foremost a human tragedy. But the global economic impacts are also coming into focus.

Events are moving fast, but at the time of writing, the main economic fallout will be from a severe shock to commodity markets. We think higher commodity prices are here to stay and will lead to both higher inflation and lower growth. This means the risk of outright recession in Europe is rising sharply, especially if physical commodity flows from Russia are substantially disrupted in the coming days and weeks.

Unenviable choice

The Fed, the ECB and Bank of England were already wrestling with higher inflation and slowing growth. The Ukraine war has not changed those fundamentals, but it is likely to exacerbate both. Policymakers are facing an unenviable choice between acting hawkish to get inflation under control at the risk of meaningfully damaging growth, and letting inflation run unchecked in order to protect growth as much as possible.

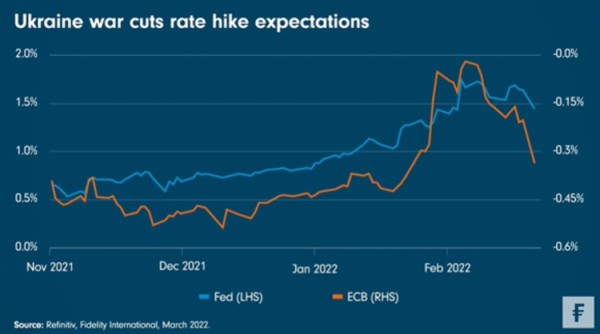

For the US, the shock is predominantly supply-side driven, with knock-on implications for inflation expectations. Oil is the primary channel by which the war will impact the US economy and inflation now appears likely to peak in Q2 rather than Q1. We still expect the Fed to hike three or four times this year, however the coming stagflationary shock will make policymakers more cautious. An aggressive schedule of as many as six or seven hikes in 2022, priced in by markets as little as a week ago, now also looks unlikely, given the elevated risk of recession that such fast tightening could trigger, coupled with the constraints of very heavy debt burdens.

For the ECB, however, the situation is more complicated. Disruptions to gas supplies will cause a significant shock to the continent, and the bar for the ECB to turn dovish is now low. We expect policymakers will prioritise growth. Quantitative easing is now unlikely to stop in March or June and may even be expanded. The severing of many financial links with Russia should be manageable for Europe, as the region’s banks are flush with liquidity and their higher capital buffers reduce the likelihood of a ‘financial doom loop’. That said, the severe growth risks facing the Eurozone are real, and expectations for ECB rates have duly adjusted down sharply since the conflict started.

We had previously anticipated a ‘reverse Draghi moment’ as global central banks seek to recapture their credibility on inflation. At the height of the European peripheral debt crisis in 2012, then ECB President Mario Draghi declared that the ECB was ready to do “whatever it takes” to save the euro. Market participants believed in his commitment to such an extent that in the end the ECB did not have to act.

Before the invasion of Ukraine, markets believed that central banks would do whatever it took to tackle inflation, and policymakers seemed content to tacitly condone the hawkish outlook in the hope that markets would tighten financial conditions for them. The Fed will still be sticking to a ‘reverse Draghi moment’ playbook for now, however the ECB will almost certainly have to pivot to more dovish rhetoric.

Share this post!

Related posts

-

Read more about "Nuveen: Renteverlagingen Fed raken verder uit zicht door hardnekkige inflatie"

Read more about "Nuveen: Renteverlagingen Fed raken verder uit zicht door hardnekkige inflatie"Nuveen: Renteverlagingen Fed raken verder uit zicht door hardnekkige inflatie

-

Read more about "Vanguard: AI en rente bepalen de risico's en kansen dit jaar"

Read more about "Vanguard: AI en rente bepalen de risico's en kansen dit jaar"Vanguard: AI en rente bepalen de risico's en kansen dit jaar

-

Read more about "Nuveen: Fed biedt ruimte voor nog twee renteverlagingen"

Nuveen: Fed biedt ruimte voor nog twee renteverlagingen

-

Read more about "DNB: Standing with Ukraine, strengthening Europe"

Read more about "DNB: Standing with Ukraine, strengthening Europe"DNB: Standing with Ukraine, strengthening Europe

-

Read more about "DeVere: Bank of England has no excuse to delay March rate cut"

Read more about "DeVere: Bank of England has no excuse to delay March rate cut"DeVere: Bank of England has no excuse to delay March rate cut

-

Read more about "Aberdeen: Nu inflatie in VK daalt is weg vrij voor BoE om rente te verlagen"

Read more about "Aberdeen: Nu inflatie in VK daalt is weg vrij voor BoE om rente te verlagen"Aberdeen: Nu inflatie in VK daalt is weg vrij voor BoE om rente te verlagen

-

Read more about "Schroders: Sterk herstel eurozone, maar hogere rente ligt op de loer"

Read more about "Schroders: Sterk herstel eurozone, maar hogere rente ligt op de loer"Schroders: Sterk herstel eurozone, maar hogere rente ligt op de loer

-

Read more about "DNB: Waarom de ECB de rente ongewijzigd op 2% laat"

Read more about "DNB: Waarom de ECB de rente ongewijzigd op 2% laat"DNB: Waarom de ECB de rente ongewijzigd op 2% laat

-

Read more about "MFS: ECB to hold rates stable, risks appear balanced"

MFS: ECB to hold rates stable, risks appear balanced

-

Read more about "BlackRock: ECB stuck in the middle at 2"

Read more about "BlackRock: ECB stuck in the middle at 2"BlackRock: ECB stuck in the middle at 2