Fidelity: China’s EV industry is charged for growth

Fidelity: China’s EV industry is charged for growth

Governments around the world have made green policies and investment central to their strategies to combat climate change, and China is no exception. President Xi Jinping has laid targets for China to be carbon neutral by 2060, and for "eco-friendly" cars to account for all auto sales by 2035.

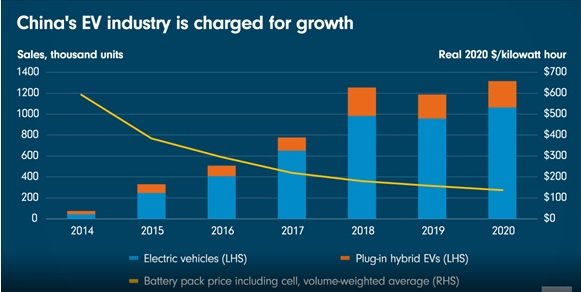

This week’s Chart Room shows how global battery prices, which are one of the largest cost inputs for EVs, have steadily decreased, amping up the growth of China’s EV and plug-in hybrid sales. Battery prices in 2020 were 13 per cent lower than in 2019, according to data from BloombergNEF, as more efficient battery pack designs were launched. China produces around three-quarters of the world’s EV batteries and is also the world’s biggest manufacturer of electric cars.

Lower battery costs and generous subsidies have sparked the growth of China’s EV industry. In turn this has boosted enthusiasm from capital markets. The entry of new players to the increasingly competitive industry will help the EV supply chain to cut costs yet further, and make owning an electric vehicle a more attractive prospect for consumers.

The road hasn’t always been smooth. China’s EV sales declined in 2019 upon the removal of some subsidies, and crashed to a four-year low in the first quarter of 2020 amid the outbreak of Covid-19. After governments around the world bolstered their commitment to green energy during the pandemic, China’s EV market is seeing a v-shaped rebound to new highs, and market expectations are still catching up. We think the penetration rate of EVs could surpass 40 per cent by 2030, from under 6 per cent in 2020.

Not all stakeholders will be rewarded equally. The increased competition in the EV market could reduce returns on capital and some companies will lose out. We think companies operating upstream in the value chain with better competitive positions are more likely to be winners. This includes leading battery companies which could benefit from greater scale, more advanced technology, and generally leading market positions.

Share this post!

Related posts

-

Read more about "Allianz Trade: Dominantie China vergroot kwetsbaarheid Europa"

Read more about "Allianz Trade: Dominantie China vergroot kwetsbaarheid Europa"Allianz Trade: Dominantie China vergroot kwetsbaarheid Europa

-

Read more about "eToro: Hoe AI China’s energierevolutie aandrijft en andersom"

Read more about "eToro: Hoe AI China’s energierevolutie aandrijft en andersom"eToro: Hoe AI China’s energierevolutie aandrijft en andersom

-

Read more about "Rick van der Ploeg: Climate transition still being undermined by misguided incentives"

Read more about "Rick van der Ploeg: Climate transition still being undermined by misguided incentives"Rick van der Ploeg: Climate transition still being undermined by misguided incentives

-

Read more about "Natixis IM: Weinig structurele uitkomst van Trump–Xi-overleg verwacht"

Read more about "Natixis IM: Weinig structurele uitkomst van Trump–Xi-overleg verwacht"Natixis IM: Weinig structurele uitkomst van Trump–Xi-overleg verwacht

-

Read more about "Bain & Company: Kernenergie maakt comeback, uitvoering blijft grootste risico"

Read more about "Bain & Company: Kernenergie maakt comeback, uitvoering blijft grootste risico"Bain & Company: Kernenergie maakt comeback, uitvoering blijft grootste risico

-

Read more about "Triodos IM: Vooruitzichten batterijopslag positief ondanks geopolitieke tegenwind"

Read more about "Triodos IM: Vooruitzichten batterijopslag positief ondanks geopolitieke tegenwind"Triodos IM: Vooruitzichten batterijopslag positief ondanks geopolitieke tegenwind

-

Read more about "Allianz Trade: Oliecrisis duwt Nederlander richting elektrische auto"

Read more about "Allianz Trade: Oliecrisis duwt Nederlander richting elektrische auto"Allianz Trade: Oliecrisis duwt Nederlander richting elektrische auto

-

Read more about "Carbon Equity lanceert Energy Transition Debt Fund I"

Read more about "Carbon Equity lanceert Energy Transition Debt Fund I"Carbon Equity lanceert Energy Transition Debt Fund I

-

Read more about "Bain & Company: Tekort aan kritieke metalen dreigt richting 2035"

Read more about "Bain & Company: Tekort aan kritieke metalen dreigt richting 2035"Bain & Company: Tekort aan kritieke metalen dreigt richting 2035

-

Read more about "Schroders: AI en energietransitie stuwen infrastructuurbeleggingen"

Read more about "Schroders: AI en energietransitie stuwen infrastructuurbeleggingen"Schroders: AI en energietransitie stuwen infrastructuurbeleggingen