Fidelity: Direct lenders take a larger chunk of smaller loan deals

One of the biggest shifts in the investment landscape of the past decade has been the rise of private credit. For its proponents, the direct lending market represents a competitively priced and readily available source of capital that isn’t reliant on the traditional syndication process, widening the pool of growth financing options available to mid-market borrowers. And for investors, allocating to alternative asset classes like private loans can bring diversification benefits and a different risk/return profile to that available in listed debt markets.

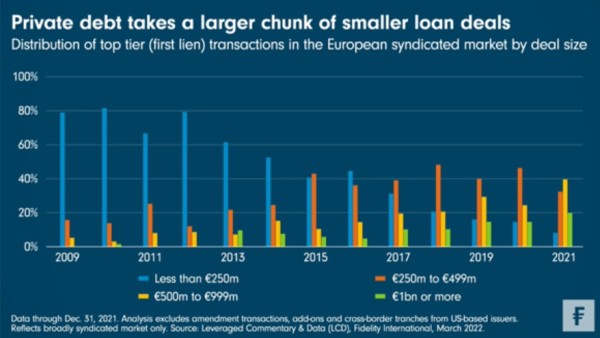

To get a sense of how big the shift has been, consider the loan market. Transactions below €250 million used to be the bread-and-butter of the European syndicated leveraged loan market. But as this week’s Chart Room shows, over the past decade their activity in this part of the market has dwindled. Instead, private lenders have stepped up to dominate this space.

By 2021, only 8 per cent of the highest-ranking senior institutional transactions in the European syndicated leveraged loan market were sized at under €250 million. The number of institutional syndicated deals of this size fell to nine in 2021 from 58 a decade earlier in 2011. The loans are still being made, of course, but the institutional lenders are being displaced by private lenders - where specific market transaction data is more opaque.

While these facilities, and the companies that draw on them, may be small, they make up a significant part of the European economy. There are over 25,000 European companies with pre-tax earnings of between €15-75 million, which account for more than 20 per cent of European private sector GDP and employment, according to Invest Europe (formerly known as the European Private Equity & Venture Capital Association (EVCA)).

With regulatory pressures in Europe leading to an ongoing retrenchment from lending by banks, direct lenders are now gaining market share to support these businesses, and managers with strong sponsor relationships, origination abilities, and investment and research capabilities are best placed to capture these opportunities.

Interest in the smallest end of the mid-market appears set to continue, with an increasing amount of deal flow coming through. While the looser terms that have abounded in the syndicated markets, such as the covenant-lite structure, have seeped into larger direct lending transactions, the smaller end of the scale is still dominated by senior secured floating rate loans with strong covenant protection.

This could prove useful in the months ahead. While there are concerns about the impact of inflation and geopolitical developments on growth in 2022, the private debt market has been relatively resilient during the pandemic and we expect it to remain so.