Fidelity: The crisis and opportunity in recycling single-use plastics

Fidelity: The crisis and opportunity in recycling single-use plastics

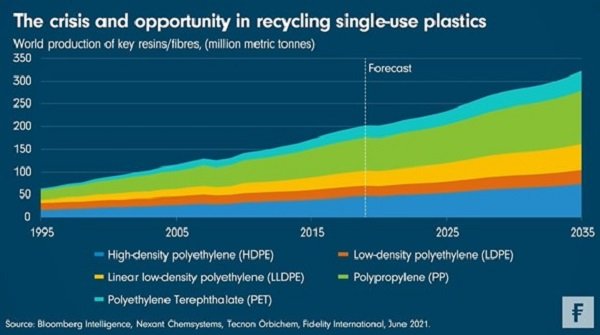

In 1950, global plastic consumption totalled only 2 million tonnes. This has increased 200-fold, to 406 million tonnes per year as of 2019 according to Plastics Europe. From an environmental perspective, the single-use plastics commonly used in packaging are a major concern, and these mainly include the following five plastic polymers according to the Minderoo Foundation:

- Polypropylene (PP) - used in things like single-use face masks, bottle caps, microwave dishes

- Polyethylene therephthalate (PET) - e.g. water bottles, bottles for cleaning fluids

- High-density polyethylene (HDPE) - shampoo bottles, freezer bags

- Low-density polyethylene (LDPE) and Linear low-density polyethylene (LLDPE) - bags, trays, food packaging cling film

And the demand for the Big Five is still growing. Usage is forecasted to grow at 3-4 per cent per annum between 2019 to 2030, similar to growth rates in the previous two decades. But in absolute terms the magnitude of increase is much greater now due to the high-base effect. For example, in the decade through 2030, the total production of these five polymers is expected to be 2.43 billion tonnes, more than during the 15-year period through 2019.

Plastics have many benefits. They are a popular material for packaging because they are low-cost, versatile, durable and light. They also bring environmental benefits such as keeping food fresh and reducing fuel consumption when transporting goods. But despite these and other benefits, plastic packaging is problematic because the way it is currently used is unsustainable and wasteful.

A crisis and an opportunity

Currently, only 24 percent of all global packaging waste is being recycled. Of the remainder, around 61 percent is sent to landfills or incinerated, where it releases high levels of methane gas and CO2, contributing to global warming. The remaining 39 percent represents ‘leaked’ or littered waste which can often be found degrading natural systems such as forests and oceans. If no action is taken, by some estimates there will be more plastic in the ocean than fish by 2050.

Demand for plastic recycling and sustainable packaging solutions is growing as result of shifting sentiment from consumers, regulators and leading fast moving consumer goods (FMCG) companies. Fidelity International’s analysts recently engaged with 41 of the top FMCG firms globally and found that 26 of these firms have specific targets to increase the proportion of plastic packaging that is recyclable or compostable. For example, Coca Cola and Nestle are among 250 major brands who have promised to eliminate all unnecessary single-use plastics and invest in new technologies so all packaging can be recycled by 2025.

Investing in the circular economy

As a result of all these trends, we estimate that ‘circular’ packaging solutions, or those relying on recyclable or compostable input materials, will grow at a consolidated annual rate of 24 per cent over the three decades to 2050, rising from 8 million tonnes to 84 million tonnes per year. With this huge investment opportunity, it is important for investors to be able to identify the key technologies and the companies that will gain first mover advantage and profitably scale.

Within ‘circular’ packaging solutions we would highlight two areas with solid growth potential: post-consumer recycled plastic (PCR), which is itself recyclable, and bio-based plastic packaging, which is compostable. Firms prefer the former because it’s cheaper, but supply constraints mean not all demand for circular plastic packaging will be able to be fulfilled by PCR plastic packaging. As a result, bio-based plastic will be required to make up the shortfall. To meet the projected surge in demand, by 2030, we predict that the PCR market will grow at an annual rate of 23 per cent (for a 9-fold expansion), while bio-based plastic packaging may grow even faster, at an average annual rate of 33 per cent.

By using fundamental, bottom up stock selection, we seek to identify and invest in the innovators that will be helping to drive a step change in the ‘plastic planet’ crisis - the companies with the leading, lowest-cost technologies that can operate at scale.

Deel dit bericht

Gerelateerde berichten

-

Lees meer over "AllianzGI: Duurzaamheid is allerminst passé"

Lees meer over "AllianzGI: Duurzaamheid is allerminst passé"AllianzGI: Duurzaamheid is allerminst passé

-

Lees meer over "KPMG: Groeiend aantal duurzaamheidsthema's gekoppeld aan bestuurdersbeloning"

Lees meer over "KPMG: Groeiend aantal duurzaamheidsthema's gekoppeld aan bestuurdersbeloning"KPMG: Groeiend aantal duurzaamheidsthema's gekoppeld aan bestuurdersbeloning

-

Lees meer over "DNB: Pensioensector zet stappen richting verankering duurzaamheidsrisico's"

Lees meer over "DNB: Pensioensector zet stappen richting verankering duurzaamheidsrisico's"DNB: Pensioensector zet stappen richting verankering duurzaamheidsrisico's

-

Lees meer over "ESG Support: Wat zijn de eerste reacties op de herziene ESRS?"

Lees meer over "ESG Support: Wat zijn de eerste reacties op de herziene ESRS?"ESG Support: Wat zijn de eerste reacties op de herziene ESRS?

-

Lees meer over "Anne Kuijken (AF Advisors): Leiden strengere labels tot duurzamere beslissingen?"

Lees meer over "Anne Kuijken (AF Advisors): Leiden strengere labels tot duurzamere beslissingen?"Anne Kuijken (AF Advisors): Leiden strengere labels tot duurzamere beslissingen?

-

Lees meer over "Rendement en impact bij duurzaam gelabelde obligaties (Ronde Tafel 'Green, Blue & Orange Bonds' – deel 2)"

Lees meer over "Rendement en impact bij duurzaam gelabelde obligaties (Ronde Tafel 'Green, Blue & Orange Bonds' – deel 2)"Rendement en impact bij duurzaam gelabelde obligaties (Ronde Tafel 'Green, Blue & Orange Bonds' – deel 2)

-

Lees meer over "De opmars en fragmentatie van duurzame obligaties (Ronde Tafel 'Green, Blue & Orange Bonds' – deel 1)"

Lees meer over "De opmars en fragmentatie van duurzame obligaties (Ronde Tafel 'Green, Blue & Orange Bonds' – deel 1)"De opmars en fragmentatie van duurzame obligaties (Ronde Tafel 'Green, Blue & Orange Bonds' – deel 1)

-

Lees meer over "T. Rowe Price: Blue bonds zijn een groeimarkt"

Lees meer over "T. Rowe Price: Blue bonds zijn een groeimarkt"T. Rowe Price: Blue bonds zijn een groeimarkt

-

Lees meer over "ESG Support: Wat betekent SFDR 2.0 voor institutionele beleggers?"

Lees meer over "ESG Support: Wat betekent SFDR 2.0 voor institutionele beleggers?"ESG Support: Wat betekent SFDR 2.0 voor institutionele beleggers?

-

Lees meer over "Invesco: Instroom ESG-ETF’s hoogste sinds 2023"

Lees meer over "Invesco: Instroom ESG-ETF’s hoogste sinds 2023"Invesco: Instroom ESG-ETF’s hoogste sinds 2023