Nikko AM: Navigating the energy crisis with an eye toward molecule-agnostic solutions

Nikko AM: Navigating the energy crisis with an eye toward molecule-agnostic solutions

Jonny Russell, Portfolio Manager in Nikko AM’s Global Equity Team, explores the clean energy transition, and the sectors and companies likely to benefit. To learn more about the team’s investment approach you can download their new investment guide here.

Has Russia lit the touch paper for the next energy revolution? Ongoing war in Ukraine will likely have long term implications for global energy markets, and perhaps the hardest decisions for politicians in the coming months will be the apparent conflict between securing cheap food and energy versus a requirement to accelerate the energy transition. Should these goals come into conflict, we expect the climate to lose out. However, there are reasons to be hopeful that a more balanced approach to policy making – a “just” transition that meets all energy goals of security, affordability and the climate – can still be achieved.

The scale of the challenge cannot be ignored

The 2022 report from the Intergovernmental Panel on Climate Change (IPCC) titled The Mitigation of Climate Change highlighted that emissions in 2019 were 19% higher than originally thought, meaning the imperative for action is even greater. The world has emitted 2,400 gigatonnes of carbon dioxide (GtCO2) since 1850, 40% of which in the last 30 years. To achieve the 1.5° Celsius emissions target by 2050, the world has a remaining ‘CO2 budget’, the allowable amount of additional emissions, of just 500 Gt. For comparison, the world emitted 400 Gt in the last decade and, despite lower energy intensity in developed countries, emissions are not going down. At this rate we have 12 years left before the CO2 budget is exhausted.

The investment required to mitigate climate change is also immense. IPCC estimates the required annual spend to be between $1-$4 trillion by 2050. This spend needs to be front-end loaded. With current annual spending estimated at approximately $750 billion, clearly this is woefully short. What makes the job even harder is that we have collectively been underinvesting in traditional energy too. Investors have been excluding the sector on grounds that all fossil fuels are bad, while proponents of environmental, social and governance (ESG) principles across the capital structure have been putting pressure on management to lower their carbon footprint, decarbonise their scope 1 & 2 emissions, and set net zero 2050 goals – while at the same time improving profits. No easy feat.

Between underinvesting in existing energy systems and not yet investing anywhere near what is required for decarbonising the planet, we estimate the total under-spend across all energy systems could be in the region of $350 billion per annum and rising. The Russia-Ukraine War has exacerbated this state of affairs, and there are no easy solutions. Immediate calls for greater investment into renewables are understandable, but nearly all of the options have significant cost. Moreover, even after ramping up renewable supply it would still be at least two years before we would be net energy positive. The simple uncomfortable truth is that these options require heavy investment in terms of money and energy.

We cannot solve an energy shortage with only promises. Demand reductions and greater efficiencies out of existing fuels are the only short-term measures available. Spiking prices and volatility are the market’s way of prompting the world to actively seek out better solutions. But the good news is that several companies are emerging that have the potential to deliver.

Investing in ‘Future Quality’ companies providing molecule agnostic solutions

Within the Nikko AM Global Equity team, the sustainability and future profitability of companies is always our priority. We focus on companies more likely to experience positive surprises in revenue and profitability in the coming years. We call these ‘Future Quality’ companies – businesses available at attractive valuations that can generate sustained cash flow growth and high and improving returns on invested capital. We are inherently optimistic about the energy transition as a key investment theme, and believe an enduring cycle of rising investment into renewable energy is already upon us.

In today’s geopolitical environment, it is likely that natural gas will play an important role in the transition to a clean energy future. Therefore, suppliers into the storage and transport of natural gas should do well, but it’s critical that their solutions are transition-ready, such as those provided by Linde. Its solutions can be molecule-agnostic and ready for a future where hydrogen plays more of a leading role. Hydrogen has been prematurely hyped in the past, but it is now at an exciting stage of commercialisation as it approaches a tipping point for demand acceleration. Scale is key for the required cost reductions to make it more competitive, but we are confident that this is now being addressed due to more state sponsored projects, ramping of capacity and wider availability of renewable energy for green hydrogen. As an example, Linde recently constructed the world’s first hydrogen refueling system for passenger trains in Bremervörde, Germany. The system’s total capacity, of around 1,600kg of hydrogen per day, puts it among the largest hydrogen refueling systems ever built.

While the return structure for the energy sector as a whole has never reached a level high enough to earn the Future Quality moniker, the energy services sub-industry has fared notably better, at times achieving exceptional returns. We expect their returns to materially improve as the best management teams have pivoted their businesses to include clean energy services that should allow them to capture significant growth in a hollowed-out industry with little competition. Worley, a leader in engineering services across the energy and chemicals industries, is one such example. It has targeted over 75% of its business to deliver sustainable solutions, including low-carbon hydrogen, in the next five years, and its services are experiencing double-digit growth at higher margins to it’s traditional business.

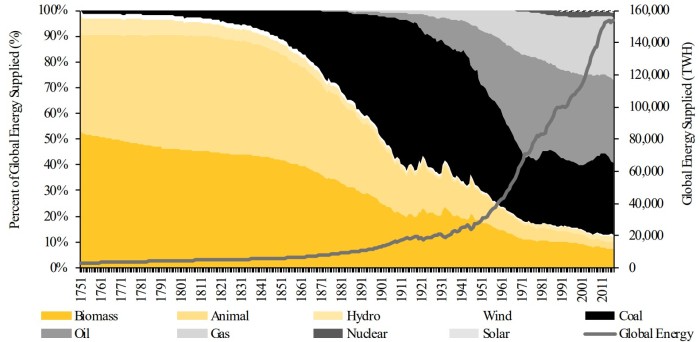

Chart 1: Energy transitions take time

We need to double down on our climate ambitions by investing in wind, solar and hydrogen while also leaning into transition fuels like natural gas, which is almost 60% ‘cleaner’ than coal and where technologies already exist to eliminate methane leaks. European policymakers have already recognised the need for this, by accepting natural gas and nuclear as transition fuels within their proposed EU Taxonomy regulations. It’s critical though that in response to the immediate crisis we build out molecule agnostic infrastructure as much as possible to future proof the assets and accelerate our transition to truly clean energy.

For the last two centuries, energy revolutions have created extensive platforms for subsequent technologies to drive wealth creation and raise living standards across the world. The clean energy transition will be no different and while the scale of the challenge is immense, the desire for change is clear, innovations are abundant, and the direction of travel has already been set.

For more information on the investment approach of Nikko AM’s Global Equity Team, and ‘Future Quality companies, please click here to download their new investment guide.

Reference to individual stocks is for illustration purpose only and does not guarantee their continued inclusion in the strategy’s portfolio, nor constitute a recommendation to buy or sell.