State Street SPDR ETF: The ECB steps up the pace

State Street SPDR ETF: The ECB steps up the pace

The ECB raised rates by 75bp and President Lagarde delivered a classically hawkish assessment of the outlook for inflation. Bond yields rose and the curve flattened as the front end priced a more active ECB. However, the EUR managed to gain little traction from these higher rate expectations. The ECB needs to remain hawkish to reduce inflation expectations. Also, despite two outsized interest rate moves, rates are still only at 0.75% while inflation for 2022 is predicted at 8.1%, falling to a still well above target 5.5% in 2023.

Jason Simpson, Senior Fixed Income Strategist at State Street SPDR ETFs:

“While the focus is clearly on inflation, growth is slowing: the July set of PMIs were all below 50, signalling the potential for contraction. This may make some of the more dovish members of the ECB cautious over how high rates need to rise. After all, if aggregate demand is already softening then there is less of a need to stamp hard on the monetary brake.

In addition, much of the inflationary impulse stems from energy prices; although, the EU is putting in place measures to control prices or at least to lessen the impact on consumers and businesses. Levels of uncertainty over exactly how high rates may go remain elevated, which makes playing bond exposures difficult.

The market currently prices terminal rates at just below 2.5% by mid-2023 but, given the low levels of conviction on how high rates may rise, caution is warranted around duration exposure. Shorter maturity investment grade exposures for Europe continues to look interesting from several perspectives.”

The case for Investment Grade

- With the ECB in the middle of its hiking cycle, driven by high and rising inflation, reducing risk through low duration strategies remains prudent. That said, the market prices a considerable amount of tightening into the front end of the curve already, which should offer some protection to shorter-dated bonds. The ECB appears to be front loading tightening and may back off if more meaningful signs of a slowdown emerge.

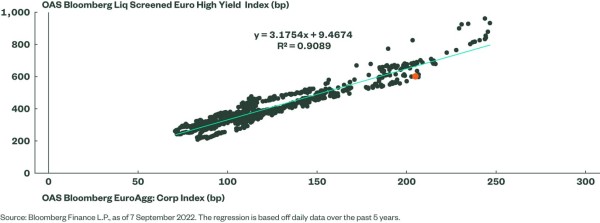

- Wider credit spreads already price an economic slowdown. The spread to Treasuries on the Bloomberg Euro Corporate 0-3 Year Index is back in the range last seen between 2008 and 2012. It is also evident that investment grade credit has undergone a more meaningful re-pricing than non-investment grade. Figure 1 shows that option-adjusted spreads on the Bloomberg Euro Aggregate: Corporates index look wide relative to the Bloomberg Liquidity Screened Euro High Yield Index based off a five-year history. The greater repricing of investment credit will partly have been driven by the cessation of purchases of investment grade paper by the ECB. Nevertheless, high yield remains far more vulnerable to a euro area recession than investment grade corporates.

- There is some evidence of a deterioration of ratings but this is not yet material. For Western Europe, the upgrades/downgrades ratio for investment grade issuers has been above one during all three quarters of 2022 for both S&P and Fitch ratings agencies. However, for Moody’s it has dropped to 0.5 for Q3, signalling twice as many downgrades as upgrades.

- The yield to worst on the Bloomberg 0-3 Year Euro Corporate index is close to 2.5%. While investors may tend to hoard cash in this type of environment, the rate paid on overnight cash is likely to be below 70bp even after the ECB’s latest rate rise.

Figure 1: Euro IG Credit spreads Look Wide Relative to High Yield

Deel dit bericht

Gerelateerde berichten

-

Lees meer over "State Street SPDR ETFs: Defence and infrastructure drive growth in industrials"

Lees meer over "State Street SPDR ETFs: Defence and infrastructure drive growth in industrials"State Street SPDR ETFs: Defence and infrastructure drive growth in industrials

-

Lees meer over "Morningstar: European ESG ETF flows in Q1 dwindle, compared to Q4"

Lees meer over "Morningstar: European ESG ETF flows in Q1 dwindle, compared to Q4"Morningstar: European ESG ETF flows in Q1 dwindle, compared to Q4

-

Lees meer over "US ETF quarterly inflows to record $ 8.87 trillion"

Lees meer over "US ETF quarterly inflows to record $ 8.87 trillion"US ETF quarterly inflows to record $ 8.87 trillion

-

Lees meer over "BlackRock: Smallcaps en zilver in trek bij ETF-beleggers"

Lees meer over "BlackRock: Smallcaps en zilver in trek bij ETF-beleggers"BlackRock: Smallcaps en zilver in trek bij ETF-beleggers

-

Lees meer over "Candriam: ECB is strengthening the case for a first cut in June"

Lees meer over "Candriam: ECB is strengthening the case for a first cut in June"Candriam: ECB is strengthening the case for a first cut in June

-

Lees meer over "La Française: No action in April but the first rate cut is coming"

Lees meer over "La Française: No action in April but the first rate cut is coming"La Française: No action in April but the first rate cut is coming

-

Lees meer over "AXA IM: ECB will cut in June, even if the Fed dithers"

Lees meer over "AXA IM: ECB will cut in June, even if the Fed dithers"AXA IM: ECB will cut in June, even if the Fed dithers

-

Lees meer over "Carmignac: ECB Preview"

Lees meer over "Carmignac: ECB Preview"Carmignac: ECB Preview

-

Lees meer over "PIMCO: ECB koerst af op renteverlaging in juni"

Lees meer over "PIMCO: ECB koerst af op renteverlaging in juni"PIMCO: ECB koerst af op renteverlaging in juni

-

Lees meer over "DWS: ECB zal de rente deze week niet verlagen"

Lees meer over "DWS: ECB zal de rente deze week niet verlagen"DWS: ECB zal de rente deze week niet verlagen