Morningstar: Understanding the Emissions Challenge for Integrated Oils Companies

Morningstar: Understanding the Emissions Challenge for Integrated Oils Companies

As the world's largest oil and gas producers, integrated oils companies are increasingly coming under pressure from investors and regulators to reduce emissions. Key to understanding the sustainability of integrated oils is determining their ability to reduce emissions to satisfy regulators and investors as well as manage its transition to a lower carbon world. There is also the risk of investors voting with their feet well before there is global governmental consensus on regulation, which is likely what integrated oil management teams view as the more immediate threat.

The latest Energy Observer from Morningstar’s equity research team looks to demystify the global emissions challenge and the actions that companies like Shell and Total can take to improve their greenhouse gas (GHG) emissions.

Highlights of the Energy Observer include:

• Integrated oils largely recognise the need to reduce emissions and have adopted targets to do so. However, on average 90% of integrated oil GHG emissions are Scope 3, those that occur during combustion as a result are beyond the companies’ control. Shell, Repsol and Total have the most comprehensive encompassing GHG reduction ambitions which include Scope 3.

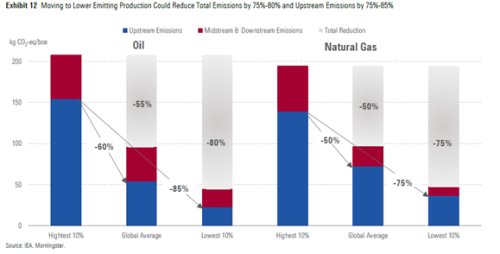

• Increasing natural gas production can help improve total emissions intensity for those seeking to do so such as Shell and Total. However, greater natural gas production can help, but alone, it won't be enough to meaningfully reduce emissions intensity.

• Flaring, which is responsible for 23% of GHG emissions, is a key opportunity to reduce emissions while increasing revenue. For integrated oils, flaring is largely an issue in the U.S. (Exxon) and Africa and Asia (Chevron, Eni). However, efforts to reduce routine flaring by building out gas infrastructure are paying dividends and we expect flaring level to continue to fall given commitments by management teams and favourable economic incentives.

• Methane comprises only about 5% of integrated oils operated emissions on average but given its greater global warming potential and opportunity for economic recovery, it’s a key opportunity area.

• Integrated oils’ ambitions to enter renewable power generation vary widely, with Shell, Total, Repsol and Equinor leading the way. Increasing renewable generation could be the most effective way for integrated oils to reduce their emissions intensity.

Share this post!

Related posts

-

Read more about "Ernst Hobma: The difference between Nick and nickel"

Read more about "Ernst Hobma: The difference between Nick and nickel"Ernst Hobma: The difference between Nick and nickel

-

Read more about "San Lie: Don't view nature as a risk, but as an opportunity!"

Read more about "San Lie: Don't view nature as a risk, but as an opportunity!"San Lie: Don't view nature as a risk, but as an opportunity!

-

Read more about "Stephan Langen: The rearguard battle around investing in fossil fuels"

Read more about "Stephan Langen: The rearguard battle around investing in fossil fuels"Stephan Langen: The rearguard battle around investing in fossil fuels

-

Read more about "Joeri de Wilde: Don't be misled by accusations of virtue signaling"

Read more about "Joeri de Wilde: Don't be misled by accusations of virtue signaling"Joeri de Wilde: Don't be misled by accusations of virtue signaling

-

Read more about "San Lie: Know and show what you own"

San Lie: Know and show what you own

-

Read more about "Stephan Langen: The sense and nonsense of benchmarks"

Stephan Langen: The sense and nonsense of benchmarks

-

Read more about "Han Dieperink: Record demand for oil"

Read more about "Han Dieperink: Record demand for oil"Han Dieperink: Record demand for oil

-

Read more about "Achmea IM: Insight into the effect of ESG on performance"

Read more about "Achmea IM: Insight into the effect of ESG on performance"Achmea IM: Insight into the effect of ESG on performance

-

Read more about "Joeri de Wilde: Anti-woke is a threat to sustainable investing"

Read more about "Joeri de Wilde: Anti-woke is a threat to sustainable investing"Joeri de Wilde: Anti-woke is a threat to sustainable investing

-

Read more about "Stephan Langen: Why wait for more green rules?"

Stephan Langen: Why wait for more green rules?